Global payments solutions for fintech and technology providers

Eliminate manual processes and upkeep so you can free up time to focus on innovation, growth, and finding value from payments.

See how WEX simplifies business payments for your customers

From virtual cards to payment delivery, as your partner, WEX offers end-to-end capabilities, including a bank, all in one place—helping you to easily deliver greater value to your customers across global markets and currencies. Give your customers better visibility, security, and even generate revenue through rebates along the way.

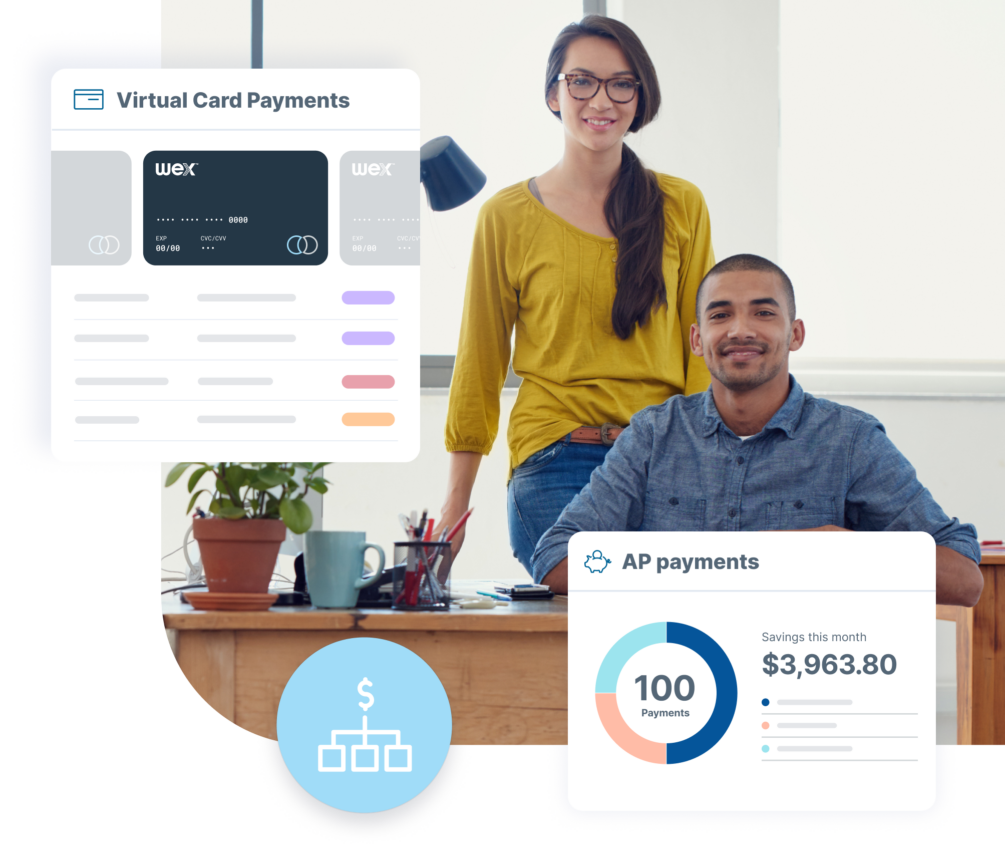

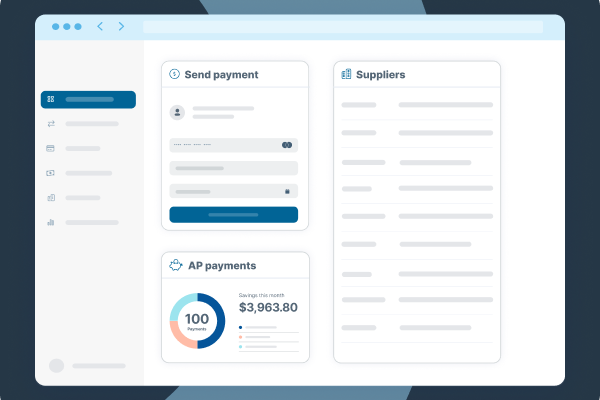

Virtual card payments

Speed the pace of your innovation and help your customers find greater value in their transactions with advanced payments technology.

With WEX payments solutions, you can generate more revenue from spend volume growth. Rapidly issue virtual cards and manage card accounts, process payments, and deliver payments all in one intuitive platform—all backed by industry-leading security, and designed for easy integration into your existing technology stack.

Full payments solution

Empower your business to change the way business gets done by working with a partner who can help you eliminate time-consuming manual reconciliation and release products faster.

As your partner, WEX offers end-to-end capabilities, including a bank, all in house—helping you to easily deliver greater value to your customers across global markets and currencies. Plus, it’s all supported by an end-to-end services team that provides technical support and data analysis to you over the life of our partnership.

Expand your payment capabilities

Launch and scale new offerings quickly with advanced payment technology

Move faster than the competition with a partner as advanced as you

Stay connected

Subscribe to our Corporate Payments Edge blog and follow us on social media to receive all our fintech industry insights.