Stay connected

Subscribe to our corporate payments blog to stay on top of payment innovations.

Payment digitization has led businesses on a quest to create more paper-free back office administration, and the COVID pandemic only served to accelerate the need for contactless payment.

For industries like travel, embedded payments technology not only facilitates reservations, ticketing and payments, but provides inexpensive and quick communications between geographically disparate departments. The value derived from virtual payments applies to hundreds of businesses and many industries.

In this article, we’ll discuss the evolution of payment technology, and how it has made businesses more efficient and created more secure processes. We also explore how converting to virtual card payments provides you with the ability to drive revenue from within accounts payable (AP).

Virtual cards work just like any physical credit card you’re used to with some added benefits. However, only 38% of United States and Canadian businesses are using virtual cards to make or receive payments from their business partners. Of those that have integrated advanced payment technology into their operations, most cite improvements across the board and in a variety of different ways.

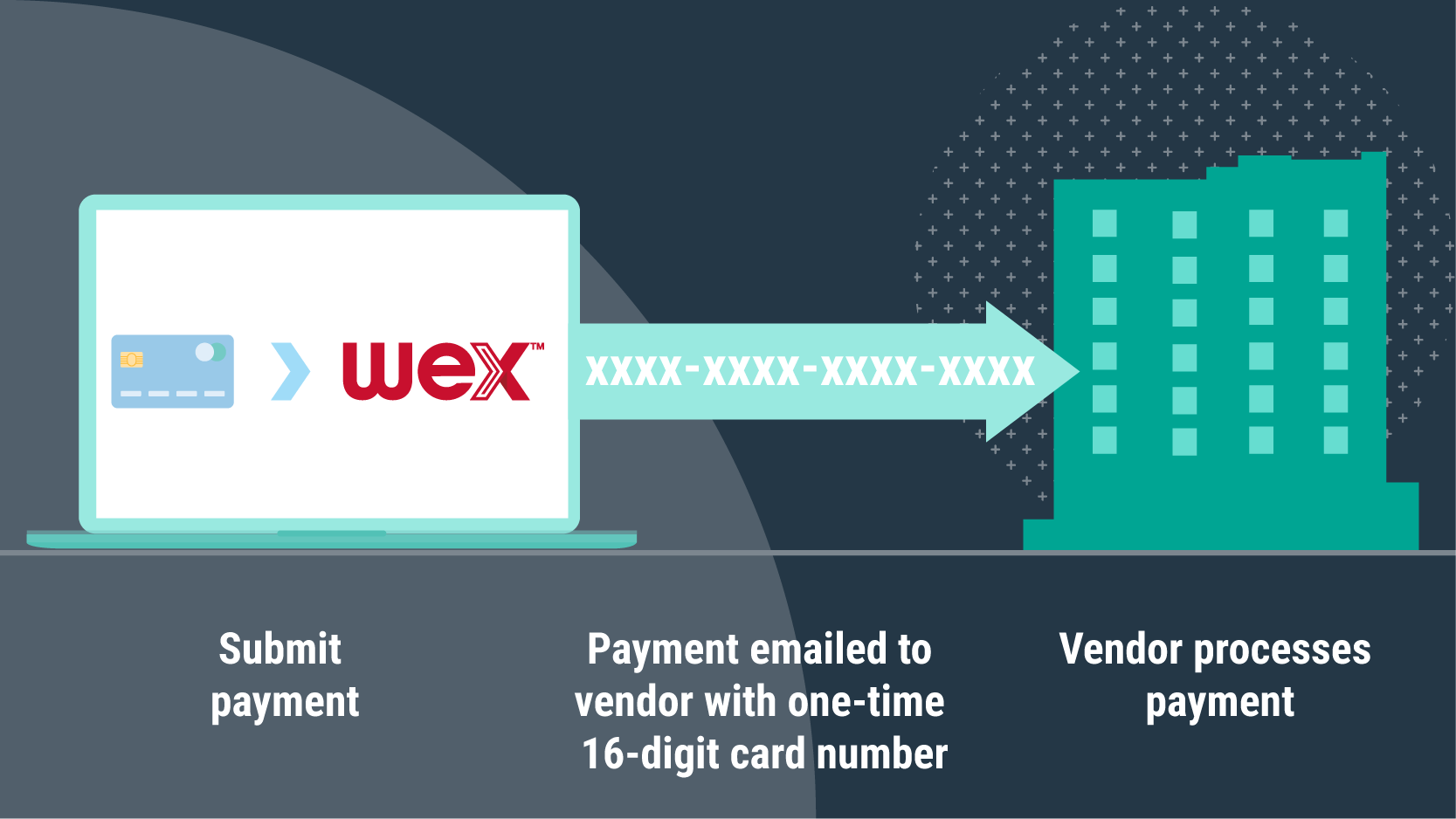

For B2B payments, virtual cards are typically randomly generated, 16-digit, single-use credit cards used to pay a specific invoice or set of invoices.

But why all the fuss about virtual payments and payment technology? Well, the cost of payment processing has long been borne by the business owner. Processing fees, back office paperwork and the cost of inefficient, manual workflows all add up. Plus, these roadblocks open the business up to potential errors along the payments journey. In turn, these bumps in the road can affect cash flow, time management and supplier relationships.

But let’s dig a little deeper.

Virtual cards offer many benefits for businesses. Not only do they help save time and money, but they also have the potential to create brand-new revenue streams for your business.

Here’s how:

Many of the resources in accounts payable are tied up in the manual reconciliation of purchase orders, invoices, and payments. In smaller businesses, the person tasked with this job often wears many hats within the organization.

Paying suppliers in a timely fashion is vital to all businesses, and maintaining a mutually valued relationship hinges on paying invoices quickly to maintain dynamic cash flow for both parties. The challenge is that these workflows have been historically manual processes.

By integrating digital payments technology, businesses gain efficiencies that provide employees with more time to manage other, more value-added tasks.

WEX works with a business’s suppliers to ensure they are signed up and connected to the company’s virtual payment process. WEX houses an extensive database and, through existing relationships with current clients, can identify suppliers that currently accept virtual cards. This allows WEX customers to quickly assess which of their suppliers are likely to easily transition to digital payments. WEX’s work onboarding your suppliers continues after the initial push and WEX works to onboard new suppliers as part of its partnership with its customers on an ongoing basis.

By deploying a virtual AP system, staff are free for more strategic business tasks, which helps improve efficiencies all around.

Legacy, manual processes drastically slow your ability to scale business. Whether you grow through acquisition or new product development, scaling operations quickly and efficiently will be directly tied to how onerous those manual tasks are.

In addition, when you add cross-border payments into the mix, you further complicate AP workflows. When your business involves handling local currencies and catering to different payment processes, having embedded payments and virtual cards will be the difference between smooth scaling and unnecessary difficulty.

AP departments are far and away the most vulnerable to fraud — especially through business email compromise (BEC), where fraudsters target invoices and other payment methods.

The implications of fraud are enormous for your business in terms of revenue loss and the potential for an erosion of trust with customers and merchants. No one wants to notify their business partners of a data breach, because everyone in the value chain becomes compromised. This can lead to additional costs, such as changing account numbers and any associated work required to integrate the new account numbers into a transaction system. In addition, the impact of fraud can sour business relationships as quickly as poor customer service or inefficient payment history.

With a virtual card system in place, your chances of fraud are reduced. A virtual payment experience provides your business with a risk-averse solution, where a unique number is generated for each transaction. That unique number can not be used again and therefore is useless beyond the transaction for which it was generated.

In addition, the best digital payment systems integrate with a business’s suppliers so that you can make payments instantly. This process works for large merchants as well as small, local materials suppliers.

Simply put, using virtual payments reduces fraud, gives you more visibility into your costs and saves your company money.

AP departments are traditionally cost centers. However, they can be made into revenue generators by incorporating online payments and a virtual card system that enables efficiency and security.

Processing checks is costly for suppliers, as banking and processing fees can vary greatly depending on the size of the business and its financial institution. Switching from manually intensive payment processes, like writing physical checks, to automated accounting systems is an effective way to save money. The average cost to process just a single invoice in 2023 is about $10.18, which is an increase of 10% from the past year. Automated clearing house (ACH) costs are usually lower but still generate fees, which are often still borne by the supplier — and sometimes by both the supplier and the customer.

Small businesses receiving or writing thousands of checks per year are all of a sudden saddled with costs for stamps and envelopes, as well as time spent writing, mailing, collecting and reconciling those payments. With virtual payment technology, those fees are transformed into rebates and could earn your business new revenue. Plus, clients can use any rebates earned to invest in the business’s top priorities.

A virtual payment system not only eliminates fees but also generates revenue as a result of the savings afforded by paying virtually — adding to your company’s bottom line.

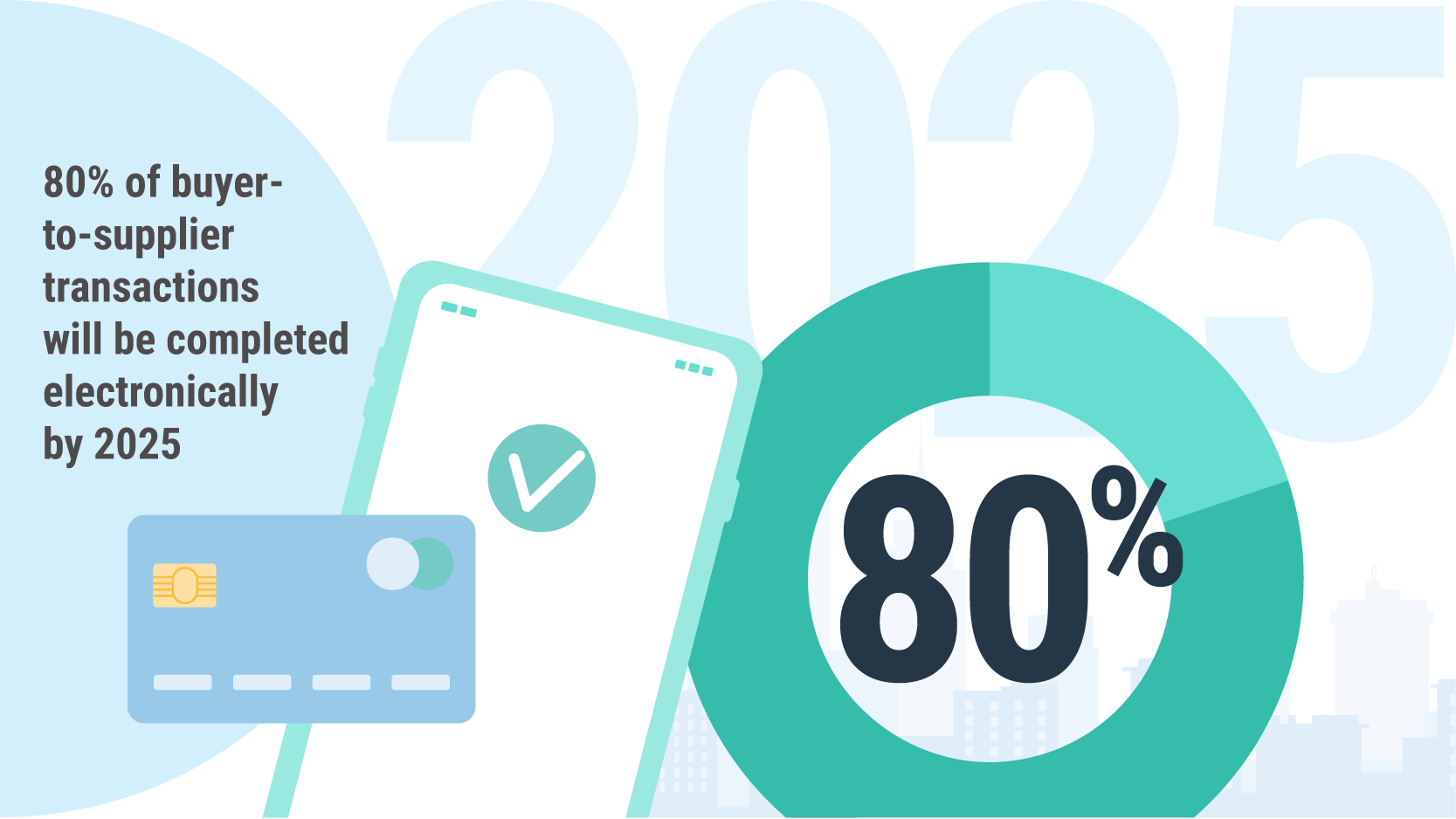

In just two years, 2025, Gartner predicts that 80% of B2B sales interactions between buyers and suppliers will be completed on digital channels. Whether your business delivers restaurant food to homes and offices or supplies copper wire to building sites, efficiency and security are increasingly tied to business success.

As some sectors embrace remote work, the ability to transact business without face-to-face interaction can be crucial. Online payments are also tied directly to risk management — be it a pandemic, extreme weather or industry action. Being able to continue uninterrupted in the wake of disruption makes for a nimble business.

Flexible, automated, virtual payment processes are a giant step toward becoming a more responsive organization.

Learn more about how WEX payment solutions can be tailored to your business, so you can accelerate and streamline operations while creating lasting growth and success.

Resources:

PYMNTS Magazine: B2B Digital Payments January 2022

Tradeshift

Pymnts.com

JP Morgan

Gartner