Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

Saving now. Planning for retirement. Investing. Participants can do a lot with a health savings account (HSA). However, the majority of HSA participants are using these accounts for short-term needs. Check out this episode of our Benefits podcast as we discuss how HSAs are being used so you can gain insight into how to best engage participants. Or keep reading to learn more.

HSAs are a valuable tool when it comes to retirement planning and investing. For those participants who are turning to these accounts as part of their long-term savings strategy, there are benefits. The average HSA balance for accounts that invest is 6.5 times larger than the average HSA balance for non-investment accountholders.

However, only about 7 percent of HSA accounts are investing. That’s why it’s important to communicate to participants in a way that resonates with whatever stage they’re at in their HSA lifecycle.

“The reality is the vast majority of people do not use health savings accounts (for retirement planning and investment),” said Chris Byrd, Executive Vice President of Healthcare Operations at WEX on our Benefits podcast. “Quite frankly, if you look across the population at the typical employer … you’ve got a whole diversity of population out there, from people who can comfortably save for retirement to people who live paycheck to paycheck.”

The Devenir 2021 Year-End HSA Report, which was just released Wednesday, March 23, included other findings, such as:

More than half of all Americans can’t pay for an unexpected expense of at least $1,000. And the inflation rate in 2021 reached its highest point since 1982. Because of that, HSA participants might be more apt to look for ways to save today.

“We’re seeing a lot of third-party research more broadly in the economy that people’s number one concern is inflation,” Byrd said.

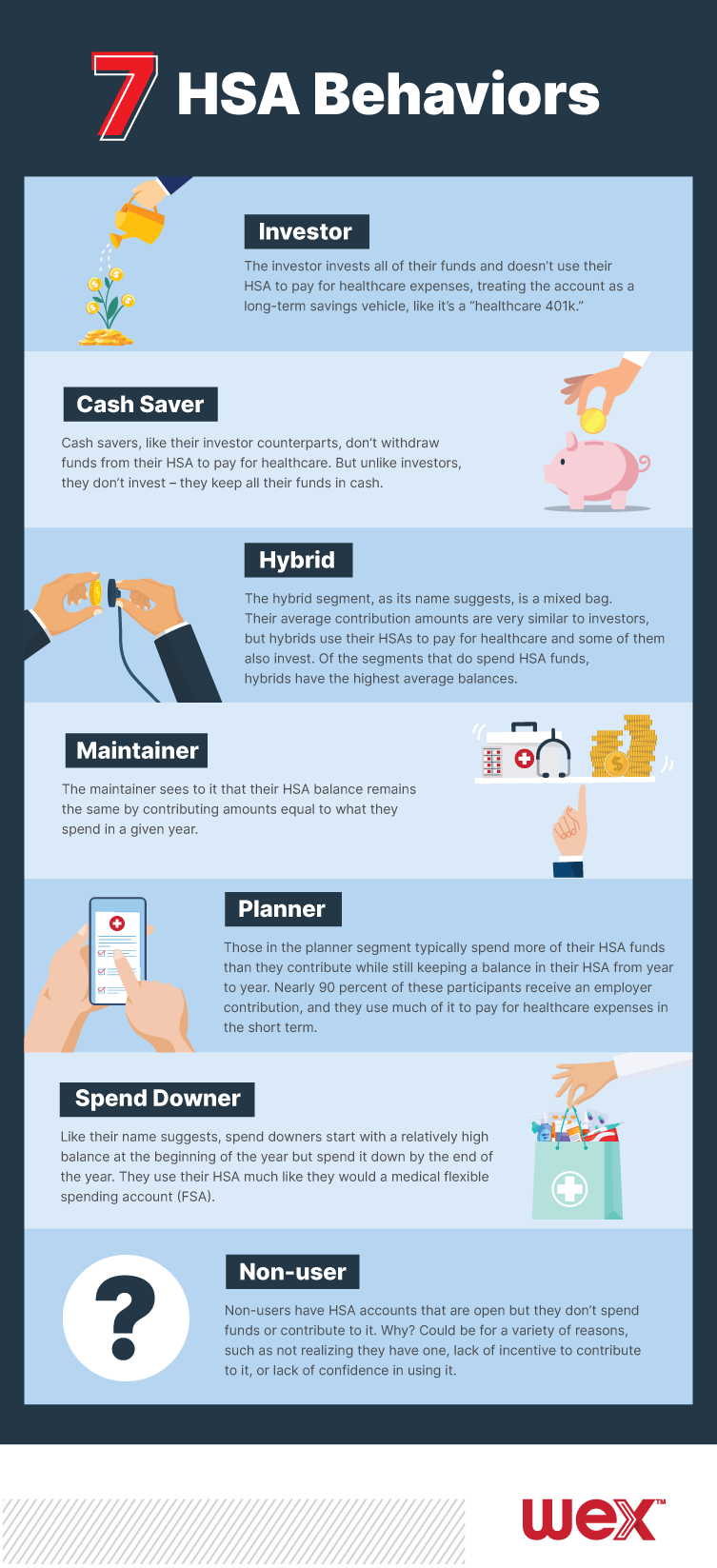

Through our research, we’ve found that HSA participants’ behavior falls into seven different segments. By tailoring messaging to each segment, you can equip the participant with the information they need to get more out of their HSAs.

It’s important to understand that these segments aren’t personas. HSA participants can shift from one segment to another, based on a variety of reasons including their understanding of HSAs, how much their employer contributes to the account, and their own individual circumstances.

Check out our infographic to learn the seven HSA behavior segments we’ve identified through our research:

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own counsel.