Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

As consumers in the Business to Consumer (B2C) space, we most often pay for goods and services with a digital payment method: think Venmo, credit card, or bank card. The Venmo service allows you to send payments and reimbursements to friends and family digitally. It’s basically a social app for paying. In 2021 it’s rare to see someone pull out a checkbook when standing at the checkout line, or even when paying monthly bills like the mortgage, or paying a friend back for dinner. In many spheres of life, we have adjusted to new, more efficient payment norms.

To get an idea of how big virtual payment transactions are in the B2C space, consider that about $150 billion moves on the Venmo platform every year, according to its owner, PayPal. That amounts to the same heft as the entire economy of Ukraine, or twice the size of Venezuela or Bolivia’s economy.

All that said, a recent survey found that more than half of all B2B payments are still made by paper check. When a business sends a supplier payment it is most often via a paper check transaction. If in our personal lives we have found easier ways to pay one another and pay our bills, why are some businesses slow to adapt to this disruption happening in payments?

WEX recently partnered with (E) BrandConnect, a commercial arm of The Economist Group, to survey several hundred executives in the financial services sector. They found that digital payments had reached a tipping point: “The findings show both opportunity and peril around payments, highlighting a stark reality: financial services companies that don’t adapt may not survive.” While the majority of businesses are still using paper check processes to make payments, that lead is narrowing.

In a five-part blog series, WEX is highlighting different key areas of their research and illuminating the opportunity and pitfalls highlighted in the report. In the first article in the series, how the pandemic accelerated digital payments transformation is highlighted. In the second article, benefits of payment technology throughout the COVID-19 Pandemic is the topic. In the third article, WEX looked at how companies can capitalize on the payments opportunities brought about by the COVID pandemic.

In this fourth article in the series, we examine how customer value is impacted by this disruption in payments.

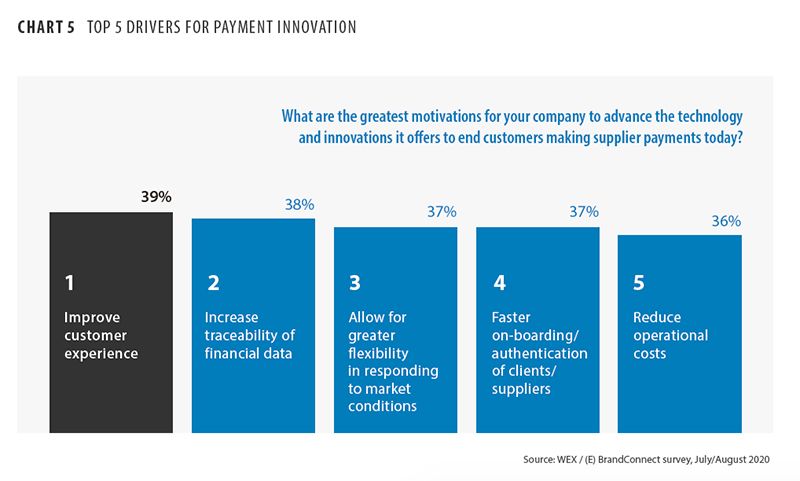

Eighty-three percent of respondents in WEX’s report with (E) BrandConnect agreed that payments innovations could deliver new business efficiencies and sources of revenue for their customers in the post-pandemic economy. A majority of CFOs and business leaders who took part in the study sought to prioritize technological changes and innovations in end-customer supplier payments solutions in order to strengthen their business. Just as many participants leveraged supplier payment technologies to innovate new sources of business value on behalf of their customers.

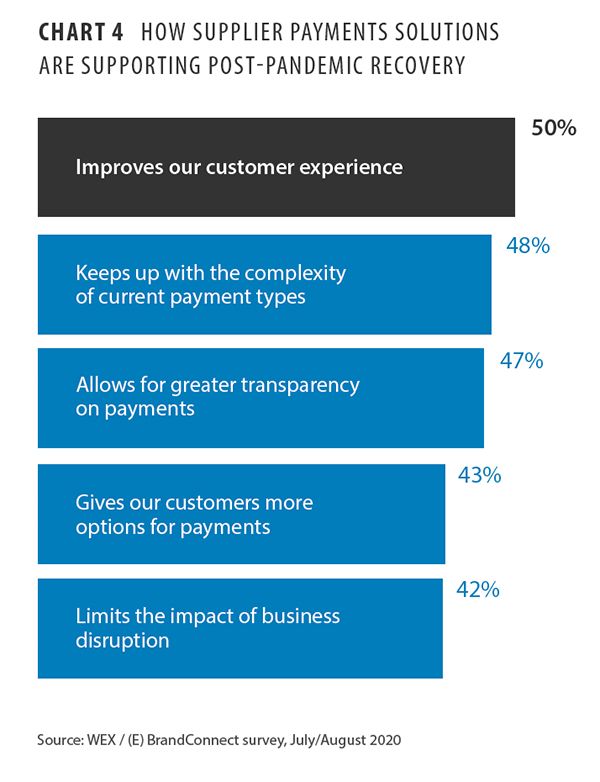

Businesses that have adapted to disruption in payments technology noted that they saw improvement in customer experience: customers enjoyed the additional information and transparency provided by digital payments.

Companies failing to convert to digital means of payments are putting their business at risk of future hardship. Globalization and more recently, the COVID-19 pandemic, have increased the necessity for remote payments. If your company is still using archaic payment processes, now is the time to convert to epayments.

There are three ways using paper checks puts businesses at risk. The first is that the more steps involved in a payments transaction, the more chances something can go wrong and the more money the payment will cost a business. For over 50% of companies still using paper checks to manage B2B payables, the additional steps to print a check and mail payment to a supplier increase risk of error—whether that’s an error in addressing a check or accounting for it and whether that’s within your own organization or within the mail delivery system.

The second is that switching to epayables will save your organization money every time you make a payment. Epayments are more cost-effective than the use of paper checks.

Finally, payments technology has rapidly evolved over the last several years. Failing to stay ahead of that disruption curve in payments could eventually put your processes out of sync with the way the rest of the world is operating, making your company less competitive and hindering its overall success.

The time and money it takes to complete the task of payment by paper check adds up quickly. The steps involved include producing the check, processing it, and fixing any issues that can be the result of human error. By removing the use of paper checks and adopting an epayables strategy, you reduce the workload of your accounts payable (AP) staff and reduce or completely eliminate the time spent:

When you adopt an epayments system, aside from the verification process (which can be streamlined when moved to a digital functionality) the steps listed above are removed and scheduling an outgoing payment in line with your monthly payment strategy becomes more efficient, less time-consuming, and more cost-effective.

As the goal of automating any business process is to eliminate the time-intensive, manual actions that enterprise departments perform on a daily basis, adopting an epayments strategy aligns with every aspect of those automation goals.

According to the American Productivity & Quality Center (APQC), accounting departments spend 49% of their time engaged in transaction processing. By increasing efficiency in the review, approval, and execution of a payment, the digitization of your payments system will give your finance teams more freedom to think and act strategically, allow for more organizational growth and give them the headspace for smarter decision making. By removing the onerous process of manual check writing and mailing, you will allow your AP team to focus on improving other aspects of the business.

In the WEX and (E)Brand Connect study, business leaders acknowledged that payments technology is still evolving and there will be a continued need for sustained innovation and investment in order to remain competitive. Only 1% of respondents believed there was no need to evolve their supplier payments. Seventy-two percent of respondents believe that they will need to continue to transform their end-customer supplier payments solutions quickly to outpace their competitors. The transformation in payments is well under way now, and will only accelerate in the coming year.

The reasons these business leaders are investing in payments transformation are:

Digital transformation is not an ambitious, solitary pursuit: it is or can be a collaboration between businesses and their service providers for the good of the customer.

Business leaders cited several negative impacts companies might experience by not adapting to digital transformations currently occurring in payments:

Global managing partner at McKinsey, Kevin Sneader, has argued that the pace of change in the current environment means that using periodic forecasts to direct company strategy no longer works. Transformation in payments technology has reengineered what customers are expecting from a payments system. By retaining archaic payment processes, businesses hinder their own ability to notice patterns and to adjust and perfect practices in real time.

“The notion that you can now forecast the economy, healthcare and other aspects of what can disrupt life, I think, is gone,” Sneader recently said. “Now we’re in an environment where we’ve also learned that what you really need to have a handle on are the metrics, insights and what’s actually happening on the ground—the dashboard of daily life.” This shift in expectations came about largely due to the rapid changes expected of businesses when COVID-19 erupted globally.

The drivers to innovate that Sneader mentions are tempered by a variety of barriers. The most common of these barriers emerge from concerns about data security/risk. Security anxieties were the most prevalent concern in the WEX study among financial services providers, which is unsurprising given the tight regulations to which these types of organizations are subject. Technology companies also expressed concern about data security.

For fintechs, however, the chief hindrance to payments innovation is tied to fragmented processes based on the countries in which these businesses currently operate. “The payments landscape is fragmented between international providers and those based within North America” WEX’s Greg Sassone, SVP Business & Partner Growth, Corp Payment Solutions, explains. “There are very few truly global providers.” That lack of cohesion among payments providers makes it difficult for fintechs to deliver seamless global service to their customers when providers are expected to craft their own solutions: fintechs rely on providers to evolve their technology as quickly as the rest of the industry, which is not always realistic in a global economy.

These specific supplier payments innovations offer the greatest value to customers, in order of priority:

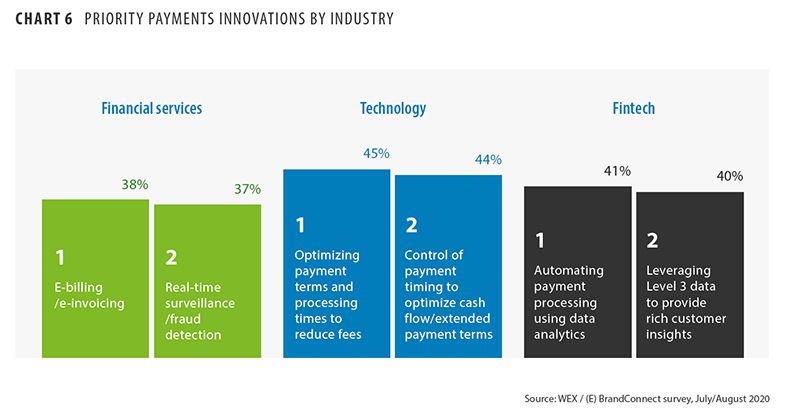

Technology companies and fintech providers have specific priorities for payments innovation. Tech companies are focused on providing their customers with more sophisticated control of payment terms and timing. For these companies, optimizing payment terms and processing times to reduce fees is the most important innovation. Secondarily, tech companies need to be able to offer their customers the ability to control payment timing. This allows their customers to optimize cash flow/extended payment terms.

For fintechs, automating payment processing using data analytics is one of the most important methods to satisfy customers’ desires. For Mike Mahklow, CEO of Blair, this automation is vital because it has a direct impact on the speed of operations for his company. “Automation is very important because you want to make sure that [processing] is as frictionless as possible and as quick as possible,” he says. Fintechs can then leverage that data for further customer satisfaction.

This ties into the second-most important payments innovation for fintechs which is the ability to leverage Level 3 (transaction) data to provide rich customer insights. The expectation from fintech customers is that a large part of the value they are getting from their relationship with the fintech is in the data and what insights will surface as a result.

The next generation of fintechs will offer value to their customers by providing meaningful insight from the data they can expertly extract through digital payments. For MoneyLion, a consumer banking, lending, and investing start-up, there is a clear link between the ability to extract insight from customer data and the ability to design experiences that deliver customer value and engagement. “We’re investing heavily in user experience as data gets better and faster to give insight,” says founder and CEO Dee Choubey.

Different sectors of the industry are providing different benefits to their customers thus their expectations of what their customers will realize from payments technology transformation vary.

Technology companies see the potential in virtualized payments technology. They expect their customers to use virtual payments technology to eliminate cross-border FX fees. They also believe their customers will use virtual cards to ensure global payment acceptance.

Financial services providers believe customers will get the most value from auto-reconciling payments and managing by exception. The fintech sector ranked use of virtual cards to ensure global payment acceptance first when asked where their customers will find the most value.

For WEX’s Mark Aquilina, SVP, Product & Strategy, Corp Payment Solutions, this difference comes down to how each group views payments. Tech companies and fintechs are looking to optimize single transactions which virtual cards can help to achieve, he explains. Financial services companies prefer to maximize the potential of a line of credit, similar to what’s provided with a conventional credit card. Reconciliation is more essential for a credit card than a virtual card because it doesn’t expire after a single use thus requiring greater vigilance against theft.

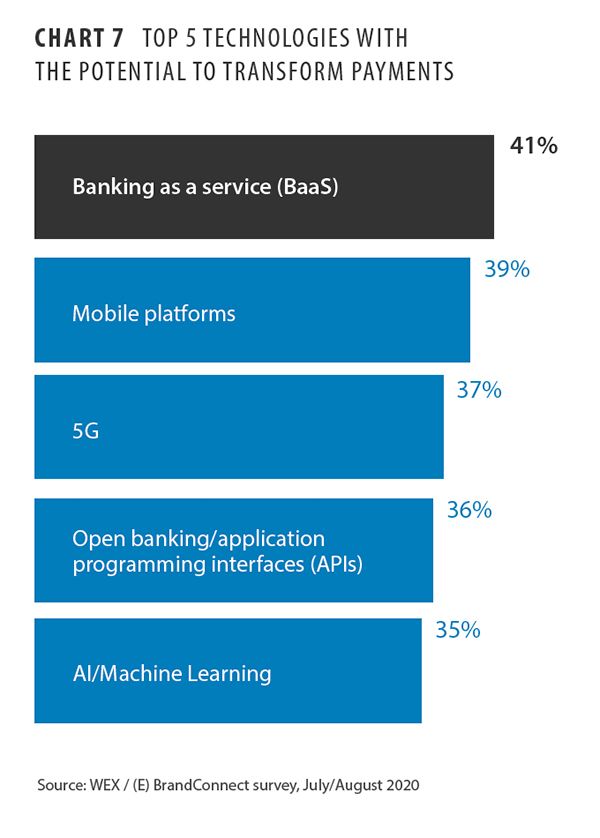

Industry-wide, banking-as-a-service (BaaS), in which banks offer white-label services that can be bundled with other offerings, is the underlying technology with the greatest anticipated impact on supplier payments.

The most impactful technology felt across the industry was cited as 5G—a foundational technology whose effect is likely to be felt most immediately at the infrastructure level.

Fintechs are an outlier on this one question of the most impactful technology that has surfaced during this disruptive time in payments, believing “AP automation” to be the most impactful as opposed to 5G.

Executives in the financial services, technology and fintech sectors all see value in supplier payments innovation, but also acknowledge the inherent risks involved.

Any payments innovation strategy requires careful planning. Consideration must be given not only to the needs of direct customers but also to their end customers. The digital transformation of payments is not a solitary pursuit, and the potential value for all participants should make this a collaborative and worthwhile innovation.

Adapting an epayments solution for your business should not derive from a one-size-fits-all approach. A generalized model will be costly and inefficient and you will incur upfront time and fees, reduce efficiencies and agility and drive unnecessary costs in the long run. Nuanced, tailored solutions exist that meet the needs of individual businesses and their employees while helping people adapt to resultant profound shifts in the workplace.

The adoption of epayments has become so widespread it is soon to become the most common form of payment in B2B. Opportunities to create new value for customers through payments innovation are clear. What’s concerning is that this inflection point could leave businesses that don’t adapt quickly enough in a state of crisis during a particularly unforgiving economic climate. As legendary value investor Warren Buffett once said: “It’s only when the tide goes out that you learn who’s been swimming naked.”

For more information on where AP stands and how epayments have helped organizations, download the WEX (E) Brand Connect report here. (Once on the page, scroll down to the “Digital Payments Tipping Point” link)

Learn more about how WEX payment solutions can be tailored to your business, so you can accelerate and streamline operations while creating lasting growth and success.

To learn more about WEX, a growing and global organization, please visit wexinc.com.

Resources:

LinkedIn

Ardent Partners

Medius

Business Insider

Time Magazine

The Economist

Editorial note: This article was originally published on December 21, 2015, and has been updated for this publication.