Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

Paying for healthcare, and paying for retirement are the two issues that are top of mind for your employees. Despite the emphasis on financial wellness, nearly half of all employees say financial stress has caused them to either miss work or has negatively affected their productivity. In any case it’s common sense that the more employees are worried about their own bottom line, the less they are focused on what they can do for yours.

What’s missing from your employee financial wellness strategy? It might be something you already offer: a health savings account (HSA). Because they’re often communicated during open enrollment with flexible spending accounts (FSAs) and other health benefits, an HSA’s true intent as a “savings” account gets overlooked. Watch our latest episode of Benefits to learn more about the value of positioning HSAs as part of a financial wellness strategy. And keep reading to see how HSAs have perks that a 401(k) and IRA don’t have.

The Employee Benefit Research Institute (EBRI) recently conducted its third annual financial wellbeing employer survey, which confirmed that “the top issues addressed through financial wellness initiatives were healthcare costs and retirement preparedness.”

Participants echoed these sentiments in the consumer healthcare report we released in 2019. In that report, nearly twice as many employees said they were stressed about their finances than were stressed about their jobs.

On top of that, the expected healthcare costs in retirement continue to rise. The average, healthy 65-year-old couple is projected to need more than $385,000 in today’s dollars to cover their healthcare costs. A 401(k) can help with these retirement costs, but withdrawals from a 401(k) are subject to income tax.

The “savings” is a key point of emphasis in “health savings accounts.” Yes, participants can save money on short-term needs. But they can also build a balance for future needs, and they can even invest their HSA funds. Plus, the purchasing and tax-advantaged power of an HSA is, in many ways, better than what they’ll experience with a 401(k) or IRA when they reach retirement.

There are a couple important distinctions when comparing an HSA with a 401(k) and IRA:

“HSAs are the one benefit that can check both the healthcare and retirement-planning boxes,” said Jeff Bakke, who is chief strategy officer for WEX’s health division. “That’s why these accounts should be the cornerstone of your employee wellness program.”

Over half of HSA-enrolled employees also contribute to a 401(k). But there’s a reason why these employees should consider maxing out their HSA contributions before they contribute to a 401(k) or IRA.

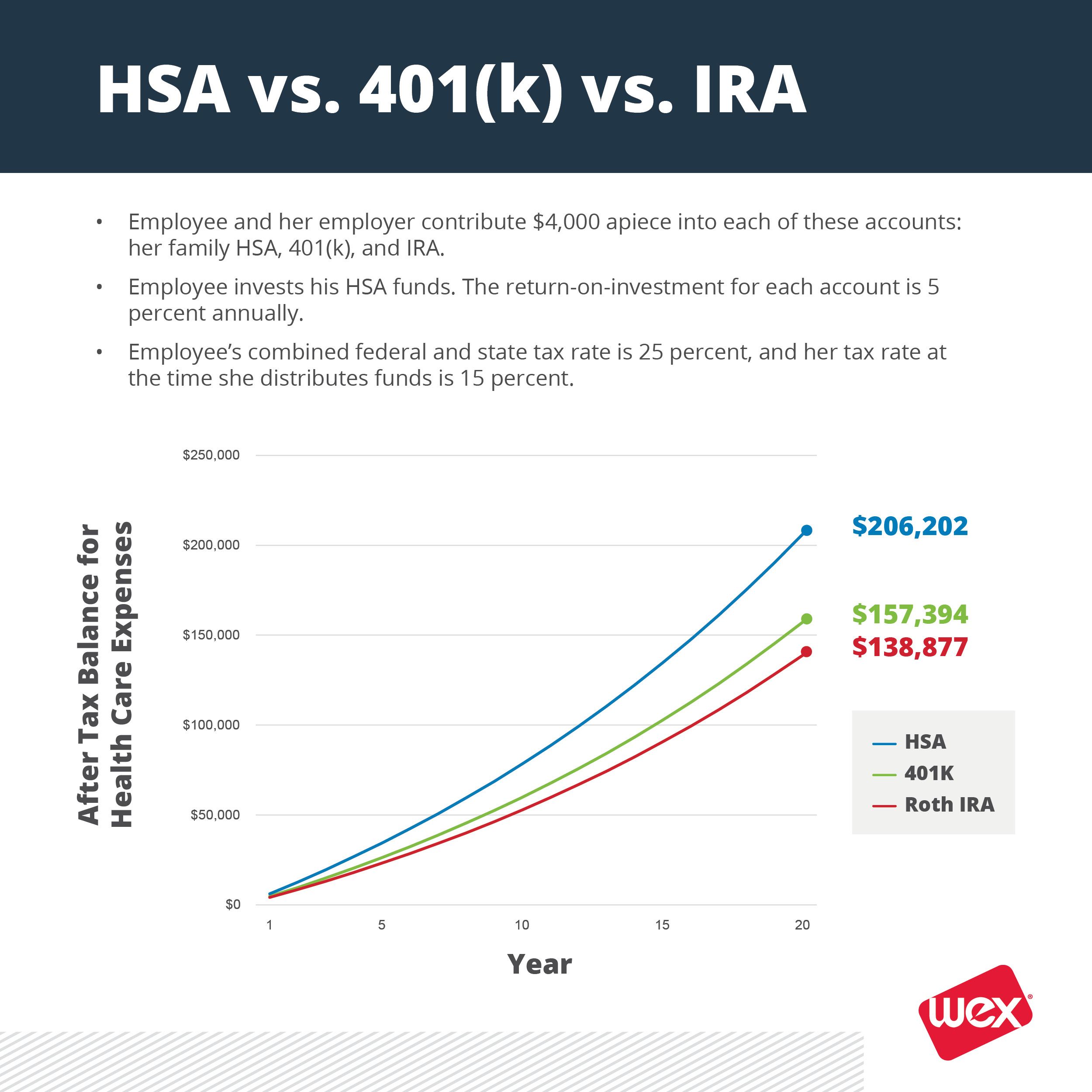

Let’s lay out a scenario for someone, who we’ll call Jane Smith. Jane is married with two kids and is preparing for retirement by participating in an HSA, 401(k), and IRA.

Watch her funds grow:

That’s a 31 percent increase in healthcare purchasing power with an HSA after 20 years when compared to a 401(k) or IRA! So what happened?

“Because of the triple-tax advantage nature of an HSA, employees actually make more money than with a 401(k) or IRA,” Bakke said. “There are other variables, such as employer matching of HSA or 401(k) funds that employees need to consider. But all things being equal, they’re actually better off putting money in HSA.”

Can you do more? Or, can you do “MORE”? Yeah, there’s an acronym for just about everything. But maybe this mnemonic device will help you remember a few things you can do to boost HSA participation.

Would you like to learn more about HSAs and retirement planning? Get your free white paper.