Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

Fraud is on the rise and comes in many forms. As reported by the Pew Research Center fraud is skyrocketing. In 2025 there was a record $196 billion in losses due to fraud as reported by the Federal Trade Commission.

Over the last several years, fraud is also increasingly difficult to detect. For those of us who’ve been in the business for a number of years, when we think of phishing, we think of something terribly written and obvious in its nefarious origins. Due to AI, what used to be transparent and detectable signs of fraud are no longer so apparent. Bad actors have become more sophisticated and their content is much more believable as a result.

Fraud is a difficult challenge when running a trucking business. This white paper will give you insights to help shore up against fraudsters and protect your assets.

The question now becomes: What do we do about it and how can you protect your business from this insidious, predatory behavior?

Most fraudsters focus on accessing cash, credit, or goods that they can resell for a profit. This can harm your business and impact your bottom line. In this article, we review the most common forms of credit card fraud and how to prevent them impacting your business.

Transaction fraud describes a couple of different types of fraud, including:

A common form of fuel card fraud happens when a bad actor obtains card data through a skimming device. Criminals install hidden devices on fuel pumps or point-of-sale terminals to capture credit card information (like card number and PIN) from users when they swipe. They “skim” the data off the card without a driver’s knowledge. They then use that information to make fraudulent purchases.

Thieves find a lost card or steal a company card and use the card for illegal purchases.

First-party fraud is both the most obvious to detect and the most difficult to prosecute. Anytime an authorized representative makes a transaction using their own identity to commit fraud, it’s called first-party fraud. What makes this fraud particularly onerous is that the user perpetrating the fraud can easily authenticate the transactions they are making. This is because they are the person authorized to use the credit. Even if an alert pops up prompting them to manually authorize the purchase, they’ll simply do so and continue with the fraudulent activity undeterred.

Here are a few examples of how first-party fraud could look in practice:

First-party fraud experiences upticks during economic downturns. This is where businesses or individuals can unexpectedly find themselves strapped and unable to make ends meet.

Identity theft can take many forms, one being account takeover. This is a type of fraud involving a cybercriminal accessing a user’s online accounts. The criminal obtains login credentials through fraudulent means, using them to illegally access another person’s cash, products, and personal account information. If there is one app or website the victim has access to that is improperly secured, the floodgates open for the cybercriminal to wend their way through connecting paths to get to other accounts and do a clean sweep of assets.

Account takeover has tentacles that reach into layer after layer of accounts causing all kinds of mayhem for the victim. This type of fraud is difficult to counteract and has far-reaching implications.

Another common form of fraud is application fraud. This is when a fraudster applies for credit using stolen or inaccurate information.

Application fraud and first-party fraud overlap. This is because application fraud often involves legitimate consumers using their own identity to commit fraud. These types of fraud are the hardest to detect because they involve the use of a true, authenticated identity.

As phishing and other types of credit card fraud increase in sophistication, here are some actions to take to prevent damage to your business:

Among these simple best practices, perhaps the most important thing you can do to avoid card fraud is educate your employees on how to be vigilant and give them the agency to decide on the fly what might be fraudulent and what to do to prevent further action from fraudsters.

Your biggest defense against fraud is your people. According to the 2024 Association of Fraud Examiners (ACFE) Report to the Nations, the median loss businesses experience due to fraud is $145,000, and fraud is estimated to impact about 5% of revenues annually. If you build a culture of education, trust, and agency, your staff will have the power to know fraud when they see it and take the appropriate steps to mitigate that activity and avoid costly impacts.

Our research shows that newer employees are better at fraud prevention and identifying socially engineered communications than veteran employees. This is likely due to fraud prevention training during onboarding that’s still fresh in their minds. Veteran employees either never received such training or could benefit from a refresher course. The best way to solve this is to make annual, mandatory fraud training part of your business plan and an expectation and priority for your staff. There is great value in constantly retraining and providing fresh information to your entire organization.

Additionally, what we’ve seen in our research is that the most secure environments empower staff to say “no” to fraudsters. Cultures where staff are most vulnerable perpetuate a fear that saying “no” to a perpetrator will mean job loss or other consequences. Fraudsters are manipulative and use menacing tactics to convert your staff, sometimes even threatening that they will lose their jobs if they don’t do what they are told. This forces your staff to take actions that allow criminals to infiltrate your systems. If you empower your staff to be cautious and not easily manipulated, you can avoid this kind of fraud impacting your business.

Here are some basic rules to teach your staff to avoid harmful phishing schemes:

A currently surging fraud trend involves receiving AI-generated phishing emails from illegitimate sources. These emails – circulated globally and crafted in a more sophisticated language – are harder to detect. It’s important to remind your employees who handle these emails that WEX will never ask for login credentials to your fuel card account over email. If one of your staff inadvertently responds to a phishing email and provides credentials to a cybercriminal, they should call WEX’s customer service number immediately (printed on the back of your WEX fleet fuel cards). Alert us that your business has been compromised, and we will take the necessary steps to mitigate any attempts at fraud on your account.

Download this infographic to learn more about Dynamic Prompt and protect your fleet from fraudsters.

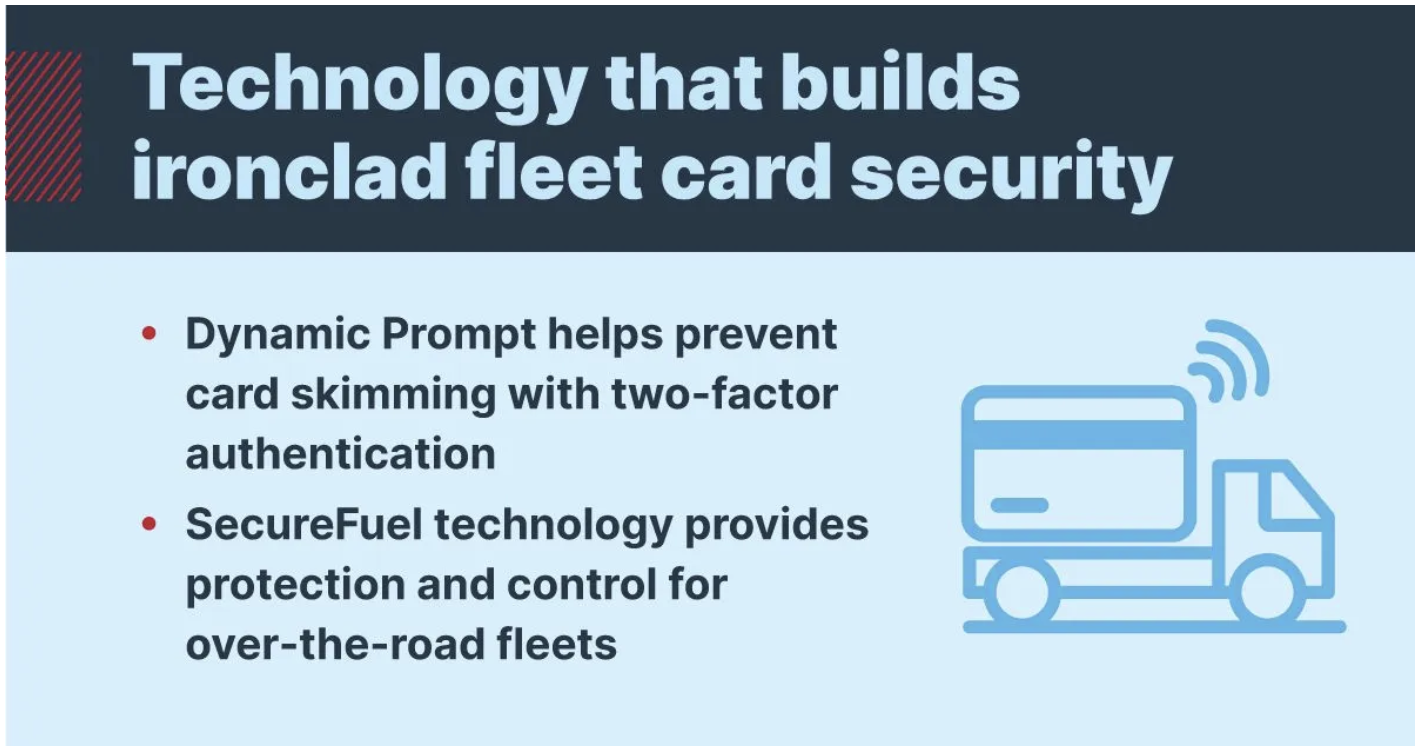

WEX has designed a security feature – Dynamic Prompt – that minimizes the threat of fraudulent activity with two-factor authentication, creating an additional barrier to prevent skimmers from being successful. This security feature helps you avoid disruption to your business and keeps your drivers moving.

Download our Dynamic Prompt infographic and share it with your drivers.

Log into eManager to learn more about Dynamic Prompt two-factor authentication from WEX.

Did you know you can add SecureFuel technology to many WEX-issued trucking fleet cards? This technology provides greater fleet card control, gives fleet managers sophisticated data reporting and telematics features, catches fraudulent behavior, and helps prevent misuse.

SecureFuel technology – which doesn’t require any hardware – integrates with a truck’s built-in telematics data to monitor fueling transactions in real time, creating more ways to keep an eye on trucks in your fleet. As credit card fraud continues to plague businesses and becomes more sophisticated, this technology can be valuable to your business.

When a driver attempts to purchase fuel with a fleet card, SecureFuel technology checks the truck’s location and tank level before securely authorizing the purchase. By combining telematics with fleet card transaction data, SecureFuel technology identifies any unauthorized purchases or misuse, and companies can choose to be notified immediately of the incident or even decline the transaction.

By combining truck telematics with fleet card transaction data to pinpoint suspicious transactions in real time – and by providing a report on the vehicle’s proximity and tank level after fuel purchases – SecureFuel can quickly find purchase irregularities and trigger an alert to your fleet manager. SecureFuel is one of the industry’s only solutions that uses the truck’s engine control module (ECM) with no additional hardware needed. Plus, as a broadly accepted solution, SecureFuel technology works at more than 16,000 truck stops across the United States.

Learn more about SecureFuel from WEX.

The following suggestions and procedures can also help protect your business from fraud:

Want to learn more about more effectively managing your trucking fleet? Explore additional WEX over-the-road articles and insights here:

Don’t yet have a WEX Over-the-Road fuel card for your trucking business? All fleet cards are not the same, and different types of fuel cards suit the needs of different kinds and sizes of businesses. View WEX’s fleet card comparison chart to see which fleet fuel card is right for you.

Sources:

Infosecurity Magazine

National Association of Fraud Examiners

Pew Research Center

Federal Trade Commission

Editorial note: This article was originally published on December 9, 2024, and has been updated for this publication.