Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

How is your HSA vs. your 401(k) vs. your IRA shaping up for retirement planning? Retirement planning is a lot easier when you imagine what you want it to be like. As Tori Dunlap of Her First $100K said at HSA Day, “I’ve gotten (millennials) to care because I have them picture 65-year-old them.”

Will you retire in Florida, or at a cabin in the woods? The average 65-year-old couple retiring today will need $395,000 to cover healthcare and medical costs in retirement. And even though Medicare helps pay for the healthcare needs of 67 million people, most recipients still spend thousands each year on out-of-pocket expenses. To help you prepare, here is a breakdown of three common retirement accounts: an HSA vs. a 401(k) vs. an IRA.

A health savings account (HSA) is a tax-advantage account that participants can pay for healthcare expenses, save for the future, and invest to build your savings. HSAs are portable, meaning that you can take it with you if you change employers and into retirement where funds may be used for non-qualified medical expenses. Employers can also contribute to their employees’ HSAs.

A 401(k) is a retirement savings plan offered by many employers that provides tax advantages. Both you and your employer can contribute a portion of your wages to an individual account. These elective salary deferrals are excluded from your taxable income, except at retirement.

An IRA is a long-term savings account that can be used to save for the future and qualifies for certain tax advantages. You can also choose to invest in a wide range of financial products, including stocks, bonds, and mutual funds, to further grow your account. An IRA is primarily designed for self-employed individuals who do not have access to other retirement savings options through an employer.

An HSA has comparable — or better — perks than a 401(k) or IRA with respect to healthcare costs in retirement. Just like with a 401(k) and IRA, you can contribute to an HSA until Medicare coverage starts. But while you’ll be taxed and penalized if you withdraw funds from your 401(k) or IRA for any reason before age 59.5, you can withdraw funds for qualified health expenses from your HSA at any time, and without penalty. Funds are available now, the HSA transfers from job to job, and there are no minimum distribution requirements. Which means employees can use their HSA to save during their working years, invest their HSA dollars, and start their retirement with a large sum set aside for healthcare expenses.

Check out our full comparison chart for more.

| HSA | 401(k) | Traditional IRA | Roth IRA | |

| Eligibility | Must be enrolled in an HSA-eligible health plan | Must be employed at a business that offers a 401(k) | Must have taxable compensation and be younger than 70.5 | Can contribute at any age if you meet certain income requirements |

| Contribution tax status | Tax-deductible | Tax-deductible | Tax-deductible if you qualify(eligibility is based

on your retirement plan at work) | Taxable |

| Distribution tax status | Tax-free (if funds are used on qualifying expenses) | Taxable | Taxable | Tax-deductible if the distributions qualify |

An HSA, 401(k), and IRA can all help employees save money when putting aside funds for retirement. All three accounts provide potential tax savings. And all three are also owned by the individual, meaning that the account stays with the employee whether they remain with their employer or not. That gives the employee peace of mind to lean on these accounts as part of their long-term strategy.

There are two important distinctions related to healthcare costs when comparing an HSA with a 401(k) and IRA:

1) Contributions and withdrawals

2) Surprise healthcare costs

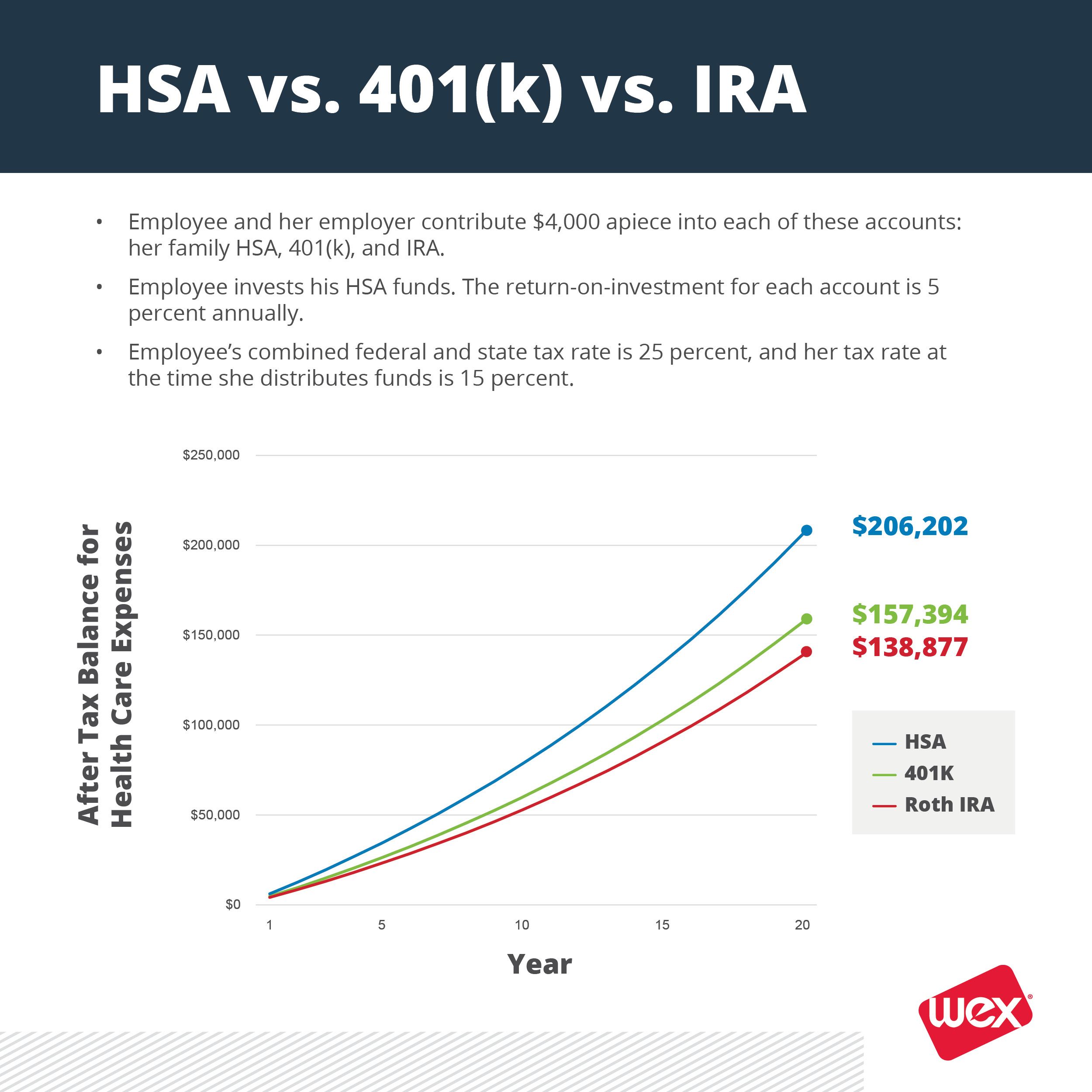

Let’s lay out a scenario for someone, who we’ll call Jane Smith. Jane is married with two kids and is preparing for retirement by participating in an HSA, 401(k), and IRA.

Watch her funds grow:

That’s a 31 percent increase in healthcare purchasing power with an HSA after 20 years when compared to a 401(k) or IRA! So what happened?

“Healthcare and retirement planning have emerged as top priorities for employers to address with their benefits,” said Matt Dallahan, vice president of product portfolio management at WEX. “One of the perks of an HSA is that it can support both of these vital employee needs.”

Would you like to learn more about HSAs and retirement planning? Get your free white paper.

This blog post was most recently updated in August 2025.

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own counsel.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.