Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

Individual Coverage Health Reimbursement Arrangements (ICHRAs) were rolled out prior to COVID-19 striking the United States, but the demand for this new product is expected to skyrocket, as more and more employers look for ways to bring stability to their healthcare costs.

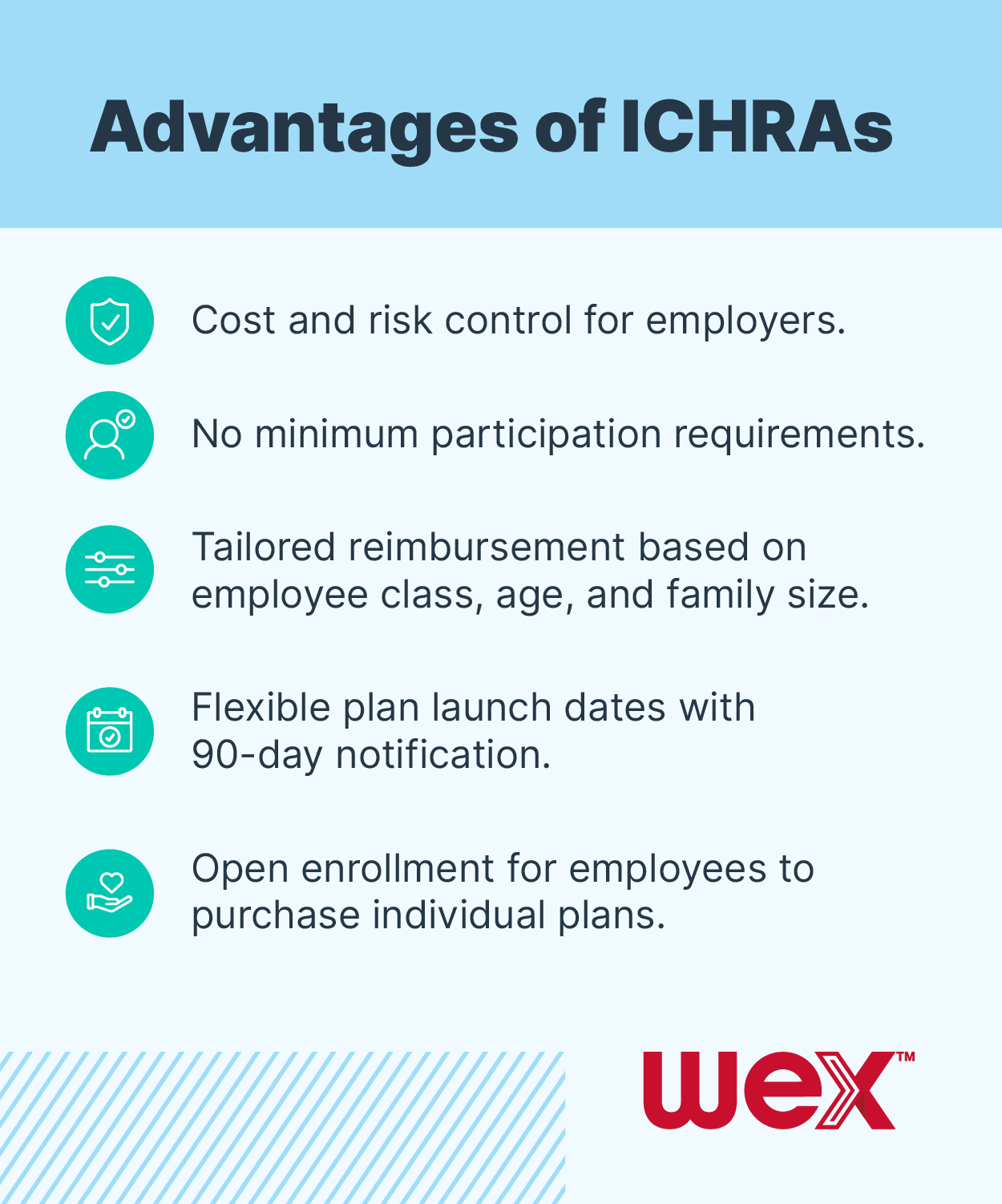

ICHRAs allow employers of any size to reduce and stabilize their healthcare expenses while also enjoying great flexibility in plan design, while employees can use them to gain a greater degree of control in their healthcare spending, tax advantages and the opportunity to receive benefits as a part-time or seasonal worker.

Want to know more? Here’s a primer on this promising healthcare benefits alternative.

Before the Affordable Care Act (ACA) was enacted in 2010, small employers commonly used HRAs to reimburse employees for individually purchased health insurance. However, regulations that spun out of the ACA halted this practice. Congress addressed the problem in 2016 with a bill creating the Qualified Small Employer Health Reimbursement Arrangement (QSEHRA), which again made it permissible for small employers to offer health insurance reimbursement benefits. In 2018, several federal departments proposed regulations to expand these QSEHRAs; the rules were finalized in June 2019. Employers of all sizes were eligible to start offering an ICHRA in January 2020.

Rather than choosing a group health plan for employees and having them purchase health coverage through their employer, ICHRAs simply reimburse employees at a set level for part or all of an individual health plan. Employers define which employees are eligible and establish reimbursement limits for each class of employee covered. Employees purchase the individual plans they want and then submit claims for reimbursement, and employers reimburse all valid claims.

These plans are tax-advantaged, exempt from both payroll taxes. And, unlike QSEHRAs, ICHRAs are available to companies of all sizes.

The health insurance premiums that employees will pay is dependent on the individual market in their state, and so the ICHRA may be more attractive to employers with a stronger individual market.

One important advantage to ICHRAs is that they allow an employer to define classes of employees that can be used to create a range of benefit levels. This is important because, unlike QSEHRAs that only allow small employers to offer individual HRAs, the ICHRA can now be used by larger employers to either cover their entire population of workers, or workers in particular classes. For instance, a large employer may want to offer a full group health plan to salaried workers and then offer part-time workers an ICHRA. Or, a large employer could offer different benefit levels of an ICHRA to different classes of employees. The classes defined in the guidance so far are:

These classes ensure that employers base reimbursements on legitimate job criteria and do not allow discrimination against, for example, less-healthy employees. However, they still give employers flexibility in deciding who can participate and how much to reimburse.

A few additional perks are that:

For more information about partnering with WEX to take advantage of this opportunity, click here.