Stay connected

Subscribe to our health benefits blog and follow us on social media to receive all our health benefits industry insights.

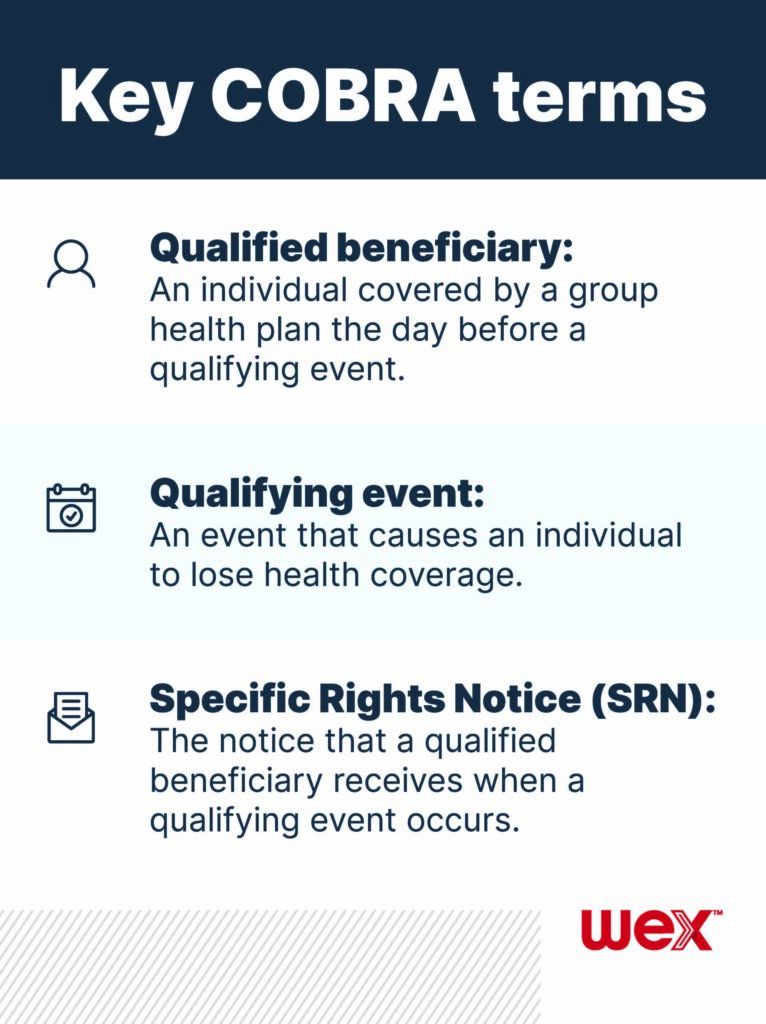

COBRA can provide important health insurance security when you’ve experienced job loss or another qualifying event. And election of COBRA can affect your ability to use the reimbursement accounts in which you were participating prior to your COBRA eligibility. In this blog post, we outline some of the ways your ability to use your employee benefits changes when you elect COBRA.

HSAs are individually owned accounts, so your HSA will stay with you no matter whether or how you qualify for COBRA. You are still eligible to participate and contribute to an HSA while on COBRA as long as:

And, if you are no longer enrolled in an HSA-eligible health plan, you can’t contribute to your HSA, but you can still spend your HSA funds at any time. Your HSA funds can be used to pay for COBRA premiums. They can also be used on group health insurance premiums if the covered individual is receiving unemployment compensation under federal or state law.

If you were enrolled in an FSA prior to electing COBRA, you may still be able to tap into your FSA funds. Your ability to spend down funds depends on a number of factors, and those factors can be specific to your employer’s FSA. You may also be eligible to re-enroll in an FSA through COBRA, but only through the end of the plan year.

Generally, claims incurred after you become eligible for COBRA are not eligible for reimbursement unless you re-enroll in the FSA through COBRA. However, if your FSA coverage ends, your FSA may have a run-out period that allows you to submit claims you incurred during the plan year for reimbursement, as long as the claims were incurred prior to the event that qualified you for COBRA.

Generally, your employer must offer you access to your HRA as part of your COBRA coverage. So, if your employer is required to offer COBRA continuation coverage, then your employer would also be required to offer the same HRA coverage to you that you elected before you experienced the COBRA qualifying event. And your HRA funds, depending on the HRA’s plan design, may be eligible to be used to pay for COBRA premiums.

COBRA provides security on health benefits, so it doesn’t include commuter benefits. For example, if your employment is terminated and you become eligible for COBRA, you would likely no longer have access to your commuter benefits funds.

Would you like to stay up to date on your employee benefits and COBRA? Subscribe to our blog to learn more!

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own legal counsel, tax and investment advisers.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.