Stay connected

Subscribe to our fleet blog and follow us on social media to receive all our fuel and energy industry insights.

So far in 2026, companies operating commercial vehicles have faced a great deal of challenges including ongoing fuel price fluctuation, inconsistent availability of vehicles and parts, and persistent ancillary cost pressures. Fleet leaders have had to rethink budgets, routes, and long-term strategies.

We sat down recently for our second set of interviews this year with Fred Rozell, President, and Denton Cinquegrana, Chief Oil Analyst, of Oil Price Information Service (OPIS), and Michael Parr, a senior advisor to the Fleet Management Association (NAFA). We revisited our Q1 reporting, and discussed our prognoses for the fleet industry in the second half of 2026, taking into account both fuel pricing and legislation.

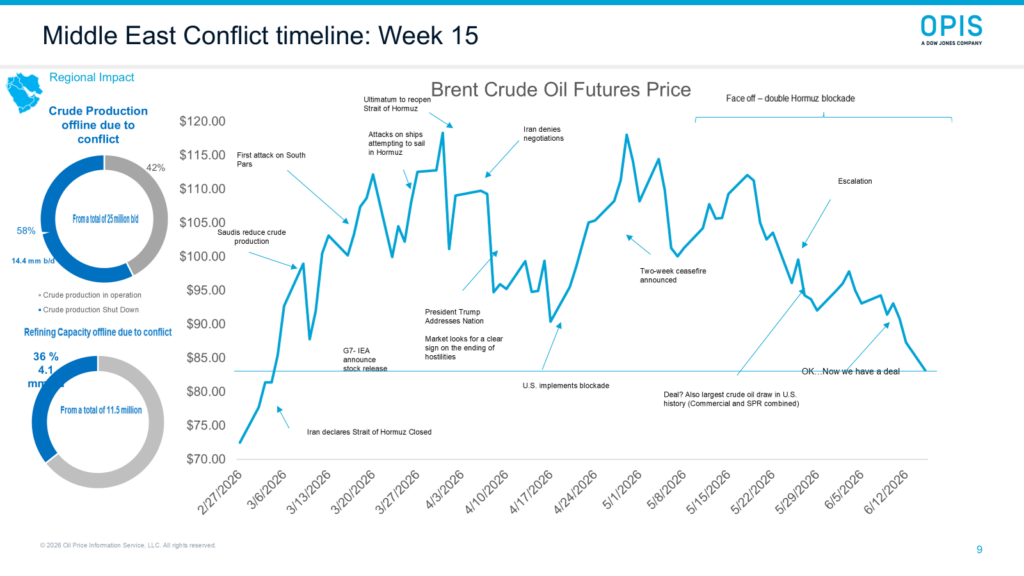

One inevitable topic was the United States and Israel’s war in Iran, initiated on February 28, 2026. As Israel and the United States bombed Iran, the government immediately took measures to close the Strait of Hormuz. The New York Times and other newspapers reported that before the war began, 25% of the world’s seaborne crude oil and 20% of the world’s liquefied natural gas passed through the strait. The closure of the straight jacked fuel prices worldwide. According to Rozell, “Even just the threat of the Strait closing causes prices to jump up.” Since February, fuel prices have fluctuated week in and week out, as reporting from the United States, Israel, and Iran has signalled either continued fighting or an end to the war.

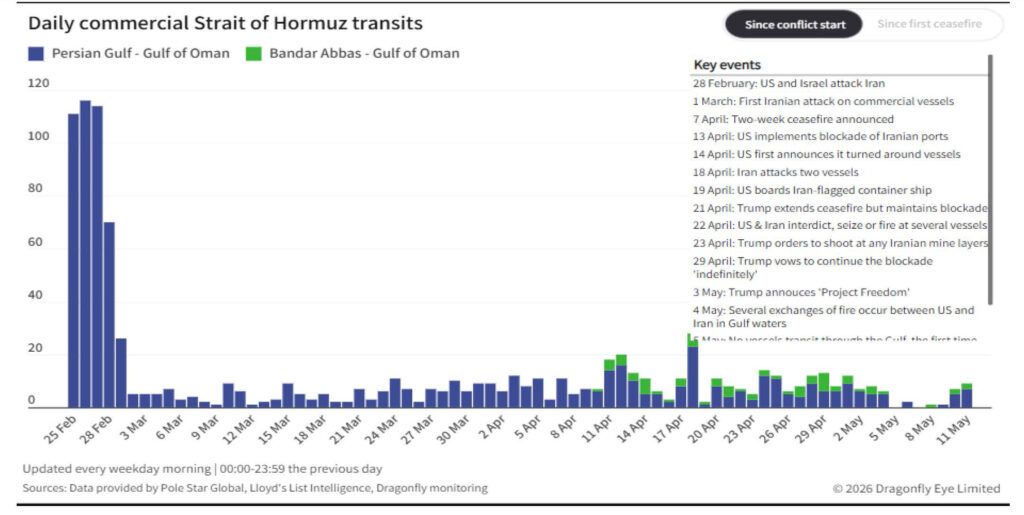

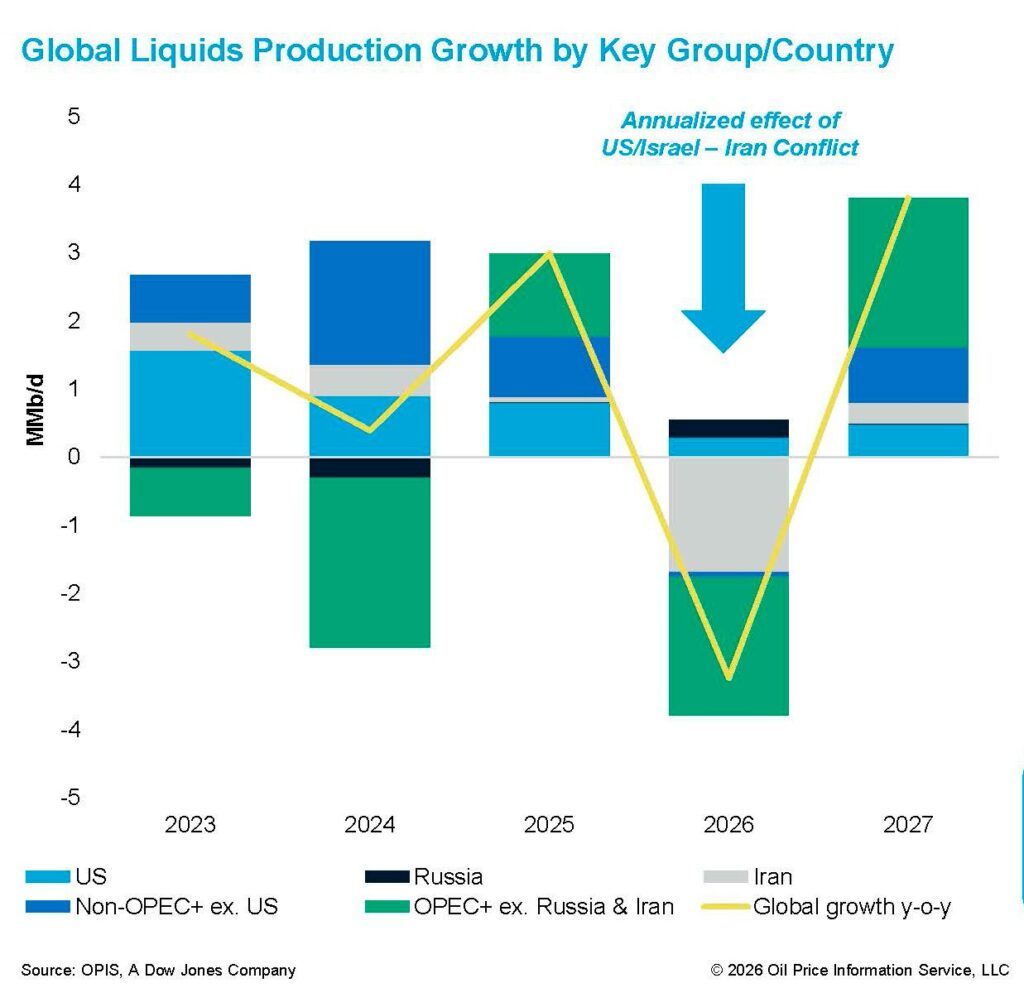

A recent New York Times article described in detail how the war has rocked the global economy. The closure of the Strait has put pressure on the sailors, the shipowners, and the operators of ships stranded in the Strait, losing hundreds of thousands of dollars a day. There are approximately 500 large vessels stranded in the Strait. According to the BBC, before the start of the war, an average of 138 ships passed through the strait each day. Between February and mid-April, according to shipping data collected by Al-Jazeera, only 279 ships passed through the Strait in total, with 22 ships being attacked. Since the cease-fire agreement signed on June 17th, the European ships in the Strait have still not moved and the number of ships passing through the Strait per-day has only risen to 55, as uncertainty around a resumption of fighting is high. Cinquegrana shared a slide illustrating the diminishment of shipments between February and mid-May of this year:

The closure of the Strait impacts industries worldwide, and fleets have adjusted predictions and shifted expectations for 2026 as a result.

The cost of fuel plays a significant role in the lives of ordinary Americans. A consumer sentiment Index is a monthly economic indicator measuring how optimistic consumers are about their personal finances and about the economy in general. The American consumer sentiment from 2019 to today has been volatile and on a steady decline. As reported by McKinsey earlier this year, U.S. consumer optimism is lower than ever: “In the second quarter of 2026, US consumers faced uneven hiring, rising inflation, and ongoing geopolitical tensions. Against that backdrop, a smaller share of consumers reported feeling optimistic about the economy, while a greater share said they felt pessimistic.”

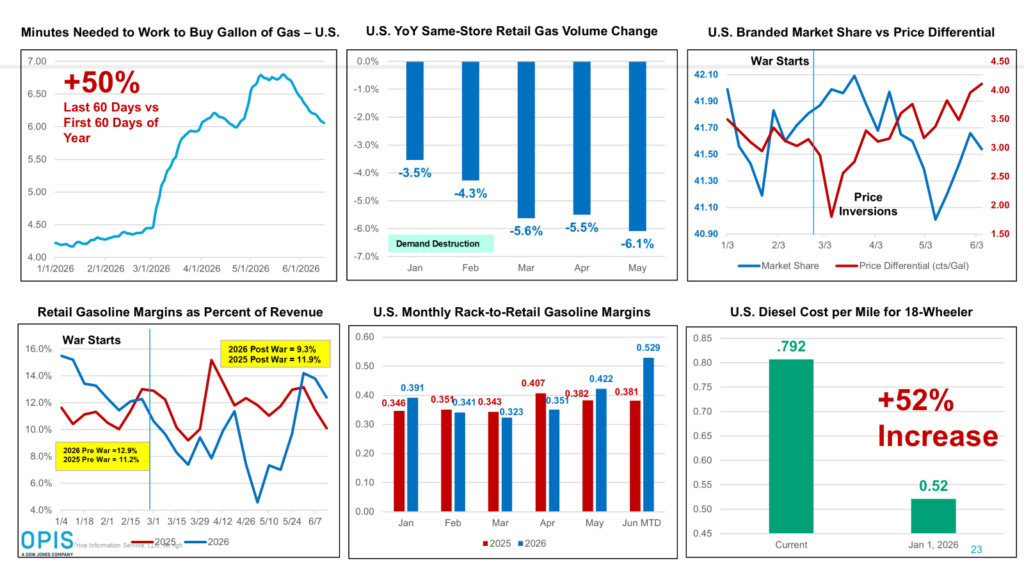

Cinquegrana illustrated the impact with the cost of fuel as a percentage of wages earned: “When we look at what it costs for the median household to buy a gallon of gas, it used to be they’d have to work for four minutes and 30 seconds to pay for a gallon of gas, now it’s upwards of almost seven minutes, this amounts to a 60% increase in the impact on families, and that’s going to be felt differently across the economic spectrum.” Businesses of all sizes are feeling the pinch, and even an end to the war in Iran will not lead to immediate economic relief.

Diesel’s price increase impact is an area even harder hit by the conflict: “If you look at the cost per mile for a diesel truck, that number has increased by 60-70% since the start of the war in Iran. This means that products that you’re shipping to stores—food, foreign-made goods, fertilizer—all of that increase in cost is passed on to consumers.” When the cost of Diesel rises, the cost of everyday goods rises with it. As Parr describes it, “Diesel price is not top of mind for the average American, but the global economy runs on diesel. Shipping, long haul trucking, trains all depend on it. So anytime you raise the cost of diesel, you raise costs across the economy. A massive amount of goods move by diesel power in this country, and there is less refining capacity for diesel than for gasoline.”

Global conflicts have affected American businesses and consumers in the past, but both Rozell and Cinquegrana noted that looking over the last hundred years, this war’s impact on fuel prices is unique. “The closest example would be the oil embargo that occurred in the early 1970s, but the world’s population in the early 70s wasn’t comparable to what it is now and U.S. petroleum markets were regulated at the time.” The U.S. government used to directly set the price refiners could charge for oil and petroleum products, regulating the industry. That changed gradually starting in 1971 with a final decontrol in 1981. Because the world’s population has grown significantly, fuel consumption has also increased. Asia’s consumption in particular in the 1970s was a fraction of what it is today. And the U.S. population has increased 67% since 1970: from roughly 203 million people to approximately 340 million today.

Oil supply from the Middle East to the U.S. is not yet causing a strain on United States fuel supplies, but Cinquegrana believes if the conflict continues much longer, that analysis may change. “That might not be for another six weeks or so, but as countries continue to come to the U.S. to fill in the gaps that they have, because they’re not getting fuel from the Strait or they’re not getting crude oil from countries in the Middle East, we may see a disruption in fuel availability in the U.S.”

The below chart shows global oil production and the dramatic dip since February:

The pipelines that run through the United States move a finite amount of oil and refined products. “The Colonial Pipeline moves about three million barrels a day. If you’re pushing three million barrels a day through that pipeline, and you’re making five million barrels a day, what do you do with those extra two million barrels? Those other two million barrels per day will go into storage,” said Cinqugrana. The issue with that calculation is that U.S. oil storage space is also finite. If the U.S. is making five million barrels of oil a day, with three sold and two going into storage, storage will eventually be at capacity. The most logical response to overproduction is pulling back on how much oil the U.S. refines and how much product is made. When storage hits its ceiling, the entire system is forced to throttle back, and when refineries ramp down they can’t simply switch back on overnight.

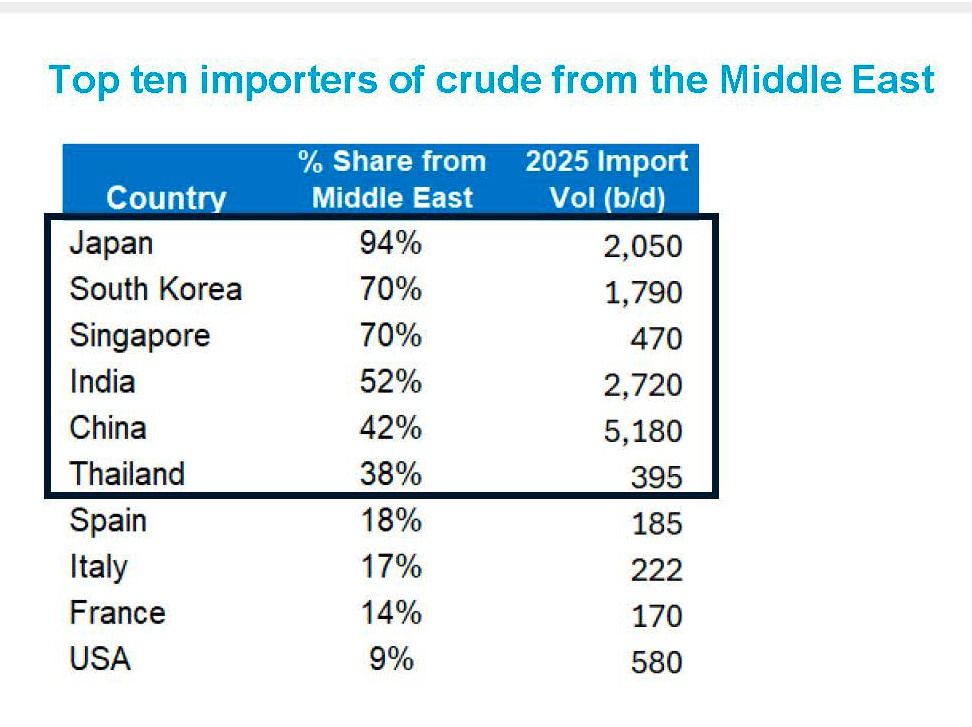

Asia has historically relied on the Middle East for over 80% of its fuel, and is by far the most impacted region in the world. Europe is not far behind. “From OPIS data you can see that Europe imports more jet fuel than they produce. Even though they produce 850,000 barrels a day, their consumption is about 1.3 million barrels a day, so they have to import the balance of that.” Those imports have historically come from the Middle East until February of this year.

If refineries in the U.S. have to reduce oil run rates, when it comes time to ramp up again they won’t be able to recover quickly. “They can’t quickly go from 30% capacity back up to 100%. It will take some time to bring those numbers back up to normal operational capacity.” On the front end, it will also take some time to reduce capacity. Given that calculation, Cinquegrana doesn’t believe restricting exports is a good idea.

Parr also made the point that some of the costs this war will incur have not yet impacted the economy. “When you look at the time it takes for an oil tanker to arrive at its destination, and for that oil to be refined and distributed, supply stabilization will not be overnight. None of the analysis I have seen suggests we’re going to see a substantial decrease in fuel cost until very late in the year, and these elevated prices might well hold on into next year.”

The long-term impact of supply chain disruption from the war has also hit Original Equipment Manufacturers (OEMs) hard. Combined with ever-evolving regulatory rules, OEMs have a lot to sift through. OEMs’ challenges have a direct impact on fleets, causing barriers to long-term planning. Parr says, “Fleets have to strategize about what vehicles they’ll need to buy in five years, and right now there’s a real lack of clarity on where the OEMs are going to go in a lot of segments. Fleet managers are unable to foresee what’s going to be available to them in the future. That is a very challenging place for their longer term planning and budgeting processes.”

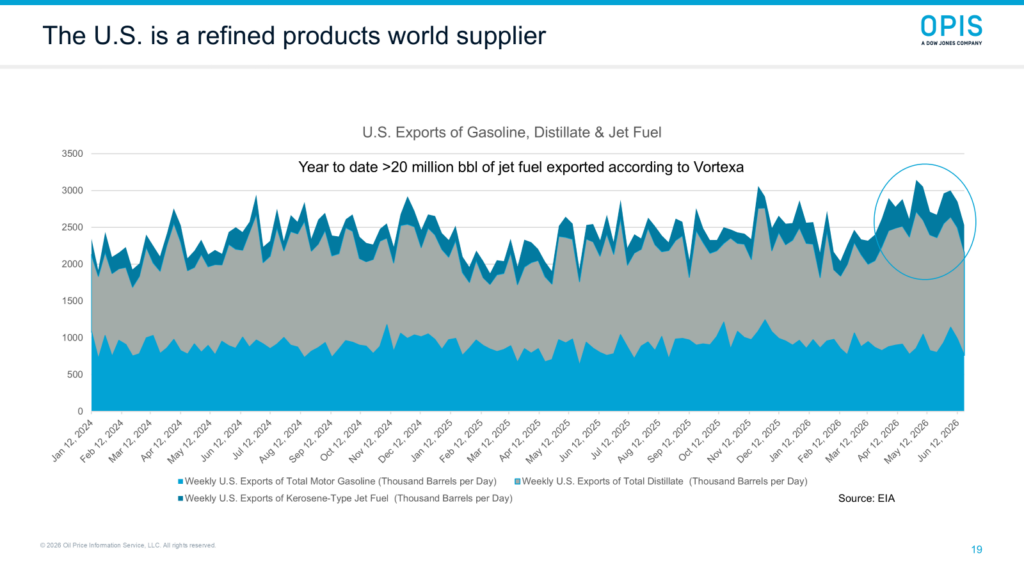

Almost immediately after February 28, 2026, Europe and Asia could not get oil from the Middle East, so they turned to the U.S. as a supplier. Between the start of the war and May 8, 2026, the U.S. saw an increase in exports and a revenue increase of about $50 billion. According to Cinquegrana, “The U.S. doesn’t currently have an oil supply problem. It has a price problem, but California may potentially have both a price and supply problem.” About 30% of California’s crude oil imports come from the Persian Gulf, with Iraq as a major California supplier. “I would say Iraq is number one, then the UAE, Saudis, and then Kuwait, but California gets probably about 70% or so of their gasoline components and blending stocks from Asia, so California is experiencing a double whammy with this conflict.” Asia supplies California with the finished gasoline molecules and the additives that are required to meet the state’s exceptionally stringent fuel specifications. That supply is also now disrupted because Asian refineries that would normally send those components to California are themselves short on Middle Eastern crude to refine.

Cinquegrana suggests California could get more supply from South American countries and Canada to solve for this issue. “Canada will also be a supplier via the Trans Mountain pipeline that goes all the way to the West Coast. They’ll be able to get imports of gasoline and components from the Gulf Coast as well now that the Jones Act was waived.”

The Jones Act (formally the Merchant Marine Act of 1920)—which was temporarily waived earlier this year— is a U.S. federal law governing maritime shipping between U.S. ports. The core rule is that any goods shipped between two U.S. ports must be carried on ships that have all of the following qualities. They must be:

The act was passed after World War I to ensure the U.S. maintained a strong domestic shipbuilding industry and a ready fleet of ships and sailors that could be called upon during wartime.

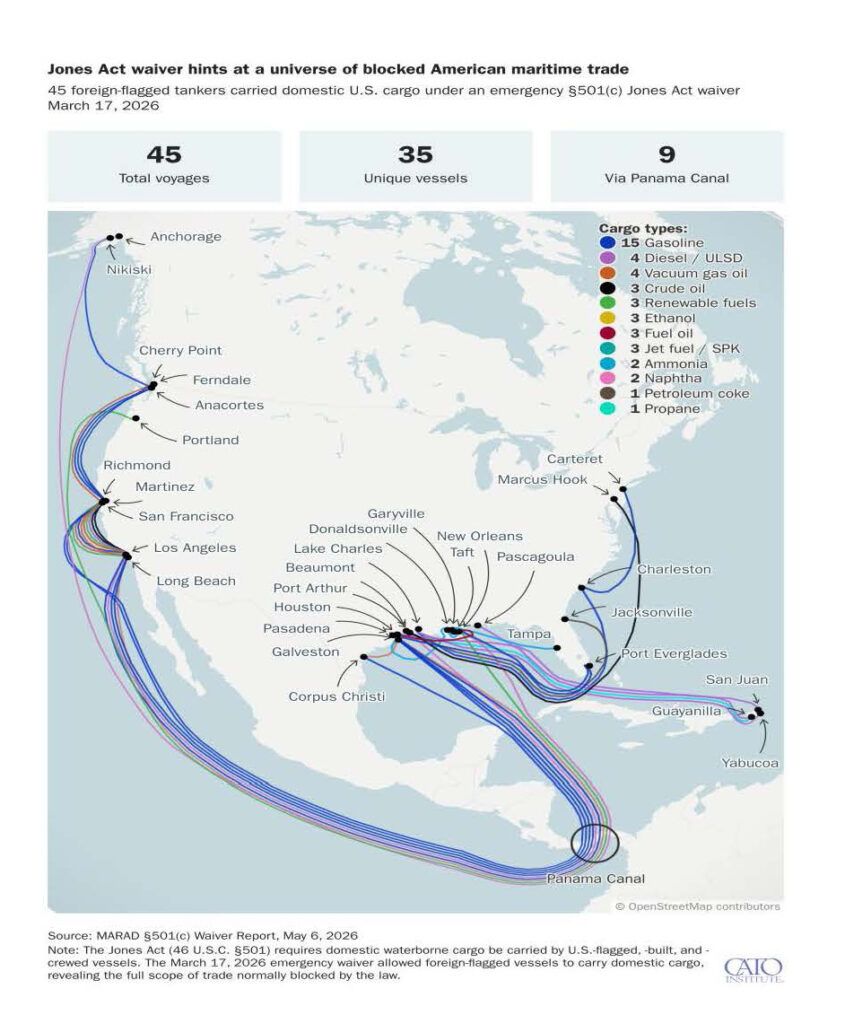

With the Strait of Hormuz disrupted, global oil rerouting has intensified pressure on the domestic U.S. shipping infrastructure. This is why Jones Act dynamics are top-of-mind for people like Cinquegrana and Rozell. See the visual below from the CATO institute of how the Jones Act waiver has impacted shipping during the Iran War:

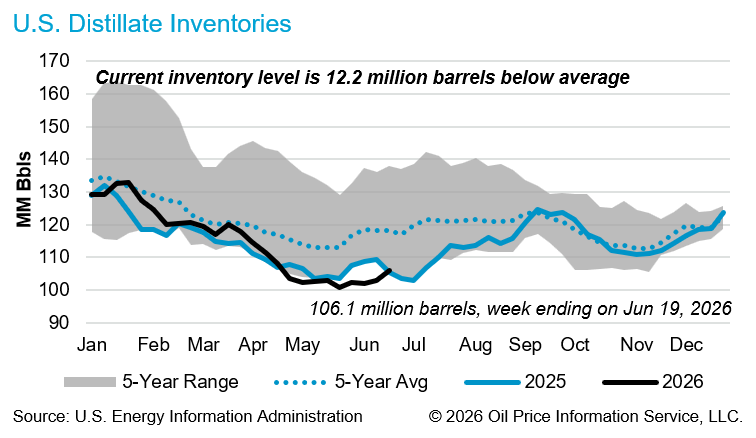

As we discussed with Cinquegrana and Rozell earlier this year, diesel inventories are diminished in the U.S. and have been since before the war began. “We’ve been operating hand to mouth with diesel for much of the last four or five years.” The convergence of factors driving that includes:

When distillate inventories fall to critically low levels it impacts the quality of fuel. There were low inventories in 2022, causing terminals and distributors to draw fuel from the very bottom of available storage. The “tank bottoms” reference in this context means:

Before the closure of the Strait of Hormuz, the finite capacity of the Colonial Pipeline to move oil, and the Jones Act’s restrictions on foreign ships moving oil both played a role in constraining companies from moving Gulf Coast diesel North by sea. This made the Northeast particularly vulnerable to tight supplies. When stocks dropped to near-record lows in late 2022, the tank bottoms quality concern became a serious issue for fleets operating in that region. Wholesale oil supply tightness translates directly into these downstream quality and availability dynamics.

The Energy Information Administration (EIA) is approaching a point now during the war in Iran where the total number of barrels of distillates will fall close to 100 million. Ninety-five percent of that 100 is Ultra-Low Sulfur Diesel (ULSD), with some higher sulfur diesels in the mix. “One hundred and two million barrels seems to be a floor over the last 5 years. This is where inventories get to the lowest operating levels that they possibly can.” When supply falls this low, it means companies will be dependent on “bottom of the barrel” oil. This is the “unwanted contents” in a barrel. When you refine a barrel of oil this is the residual fuels, referred to as “the bottoms.”

The Trump administration announced a 60-day limited waiver of the Jones Act on March 17, 2026, in response to energy market volatility amid the ongoing U.S.-Israel war against Iran. The waiver is national in scope, applying to any U.S. port. California is the biggest beneficiary, accounting for 21 of the 45 shipments completed in the first 50 days of the waiver. In the first 70 days of the waiver, more gasoline and jet fuel were moved from the Gulf Coast to the West Coast than in the entirety of 2020 through 2025.

With the Jones Act waived, Gulf Coast refiners are trying to push as much product as they can towards the West Coast because that’s where they can make the most money. The waiver allows foreign ships to step in, expanding the pool of available vessels and making the economics of the California run more attractive. “That being said, the ships don’t just automatically materialize and show up in Pad Five in Southern California from Houston,” Cinquegrana says, “It takes a while. It takes every bit of 18 to 20 days.”

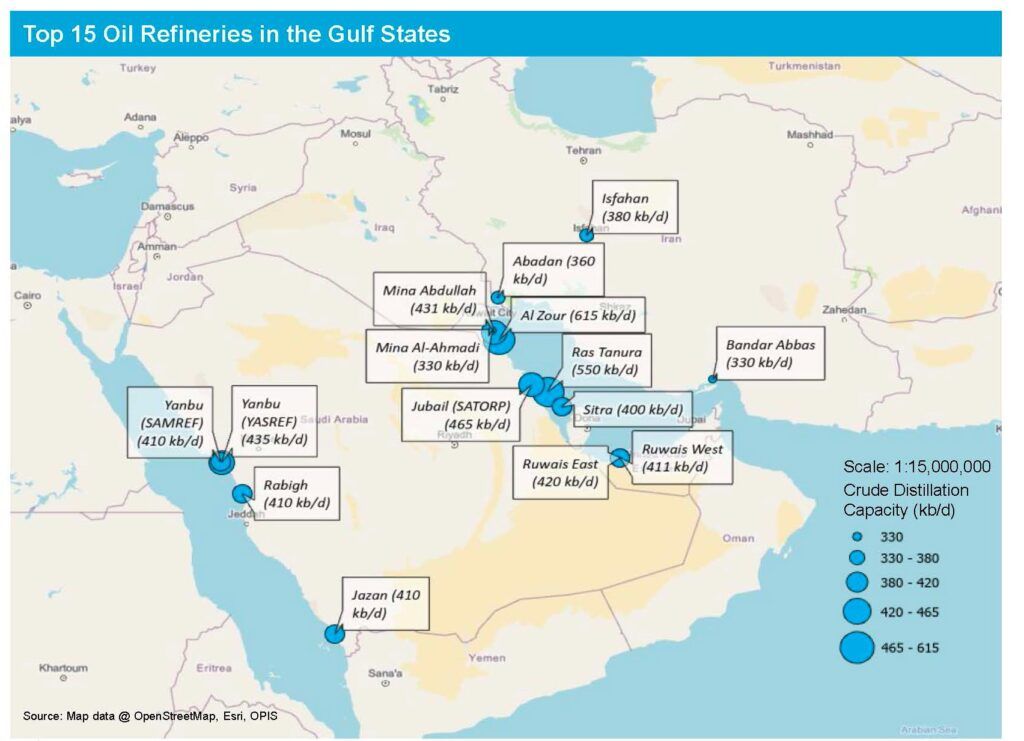

Top Persian Gulf Oil Refineries:

In early 2026, the United States launched a major military intervention in Venezuela that culminated in the capture of President Nicolás Maduro and his wife, Cilia Flores. According to Cinquegrana, Venezuela’s industrial recovery from that invasion was unexpectedly swift and comprehensive. “They’re up over a million barrels a day of crude oil production. I thought it was going to take at least a year to get there, and it’s been an almost 50% increase in production in only four months.”

For effective global oil procurement, there are three factors oil companies look for when determining whether or not to operate within a country. “For continued or increased investment the first consideration is the safety of your people running operations in the country.” Cinquegrana says, “You also need to know if you make an investment in equipment to run a refinery that your infrastructure will be secure and safe.”

The second question oil executives ask is, “Who’s in charge?” The safety of people and equipment is directly correlated to the leadership at the helm.

The third consideration for oil companies as Cinquegrana describes it, is who benefits financially from the investment. “With the Maduro regime in power in Venezuela, oil executives were forced to consider the implications of funneling profits into his government. But it’s nuanced. They could also consider the population of Venezuela as a whole benefiting from their investment. The Venezuela story is a good one, in that it’s going better than probably was originally anticipated, and probably a little quicker than anticipated.” Cinquegrana and Rozell argue that Delcy Rodriguez’s governance has inspired greater confidence in U.S. refiners, particularly those based on the Gulf Coast.

When U.S. refiners operate between the Gulf Coast and Venezuela, they only need to travel 7-8 days to transport crude oil from Venezuela to refineries on the Gulf Coast. All other available options require much longer travel times, increasing costs.

Petroleum has been a known resource globally for centuries, but oil drilling did not start in the U.S. until 1859. John D. Rockefeller and his Standard Oil Company led the charge, gaining a monopoly on oil production by the 1880s. Oil use in Venezuela dates back to the 1400s when native Venezuelans used it for both medicinal purposes and for torch fuel. Once commercial oil drilling became a profitable venture in the U.S., Venezuela saw the profit to be had and quickly joined the race to drill and refine oil.

Oil is found in three regions in Venezuela. Venezuelan petroleum deposits are located in the Maracaibo and Orinoco basins between the Sierra de Perijá and Andes mountains. The Maracaibo basin, historically Venezuela’s most productive region, is centered around Lake Maracaibo in the Northwest. The Orinoco belt, in the southern strip of the eastern Orinoco River basin, houses the richest oil reserve in Venezuela today. Exploration from 2007 onward revealed that the Orinoco Belt has more than 300 billion barrels of accessible heavy oil. The third Venezuelan petroleum-rich region is the Falcón region containing small quantities of oil in its northern reaches.

American oil companies were first in South America many decades ago. As early as 1863 a U.S. oilman applied to drill in Venezuela. The U.S. government’s removal of Maduro from power, and subsequent encouragement of more investment in the region may result in more U.S. oil companies operating there. While Chevron has been holding licenses to drill in the region for some time, Exxon has no operations there, nor do they appear ready to build infrastructure in Venezuela. Cinquegrana provided some context: “Trump recently held a press conference with a panel of oil executives about Venezuela. That’s when Darren Woods, the CEO of ExxonMobil, said, ‘Yeah, it’s uninvestible.’” This was only a week after the U.S. deposed Maduro, so there is still the possibility that sentiment will shift.

ExxonMobil has a sizable investment in oil infrastructure in Guyana, a neighboring country to Venezuela. “At times Venezuela and Guyana have argued over territorial waters. ExxonMobil has laid their hat down in Guyana and built up production there, and they’ve been burned in Venezuela before, so maybe they don’t come back, and they just put all their eggs in the Guyana basket. It’ll be interesting to see who else enters Venezuela,” shared Cinquegrana.

There is ongoing, shifting geopolitical tension between the key oil resource providers, Venezuela, Iran, and Russia. “If Venezuela returns to the world market, you’ve just cut off one of China’s sources of discounted oil.” Cinquegrana’s theory is that if Venezuela surfaces as a viable provider in the oil market they will no longer need to discount their prices to attract buyers. With the Strait of Hormuz closed, Iran isn’t exporting at capacity, and Russia continues to be constrained by sanctions. China is dependent on inexpensive oil from Venezuela, but with Iran and Russia stymied that price will not likely stay low. “Perhaps Trump’s play is to cut off China’s cheap oil sources.” By squeezing all three of those sources simultaneously, China will be forced to buy oil on the open market at market prices. China is far less dependent on oil in general though because they have invested so much in renewable energy.

The Jones Act waiver and resultant Gulf Coast shipments of oil up to California could potentially buy American companies time to shore up oil supplies to get through the rest of 2026. However, ships take 18 to 20 days to arrive in California from the Gulf Coast, and the pool of available vessels is finite. A more durable solution involves expanding California’s infrastructure. Cinquegrana shared that several pipeline projects are in various stages of development that could meaningfully change California’s supply picture over the next few years.

The most significant proposed project is the Western Gateway pipeline, which would originate at the Borger Refinery in the Texas Panhandle and run from there all the way to Southern California. An open season is the process by which pipeline operators gauge committed shipping interest before moving forward. The open season for 2026 pipeline shipments closed on March 31 with strong participation. This was seen as an encouraging signal to oil experts. A committed shipper agrees to move a fixed volume on the line at a preferred rate, even if they do not ultimately use their full allocation in a given cycle. Non-committed shippers can access the line at a higher rate on a spot basis. Getting enough committed shippers to fill the pipeline’s 200,000-barrel-per-day capacity is what makes the business model work. Strong open season interest suggests the market sees real demand for this route. That said, Cinquegrana has a more conservative, and probably more realistic expectation for the timeline: permitting processes and right-of-way negotiations could push completion into the future as far as 2029 or 2030.

A faster option than the Western Gateway is a pipeline reversal. A pipeline reversal does not mean literally pushing oil backward against the flow of a pump, it means reconfiguring the infrastructure so the pipeline, which was built to move product in one direction, is physically modified to move it in the opposite direction. This would switch the flow of an existing pipeline and send oil in one example from Western Illinois to Southern California. Reversals are significantly less complex than new construction. The infrastructure already exists, it just needs to be redirected. There is also a shorter reversal in consideration with the existing Phoenix-to-Los Angeles line. That reversal could unlock additional barrels on a similar timeline.

The takeaway for fleet managers is that California’s supply constraints are real and will not be solved quickly, but the infrastructure investment currently underway signals that the market is adapting. For fleets operating in the region, the next 12 to 18 months will be the period of greatest exposure. After that, the supply picture should begin to improve meaningfully.

Cold weather demand spikes did materialize as Cinquegrana and Rozell predicted when we last met, with a cold winter, and a relatively cold spring. OPIS is predicting we might see increased diesel demand this summer, and we may see some diesel demand for air conditioning as well. They explained that the chance of that happening is relatively small, but it’s something to keep an eye on. Winter 2026-2027 cold weather demand forecasts are not yet widely published with forecasters still focused on the current supply crisis.

Used EV sales surged by 35% in 2025, driven by consumers in search of relief from high fuel costs. Cinquegrana points out that “Outside the U.S., Chinese BYDs are available, and they’re inexpensive, and well-made.” A recent Wall Street Journal article described Americans traveling across the border to Mexico and Canada to purchase BYP EVs and hybrids, since they are unavailable in the U.S. For Americans who have not yet caught on, Parr predicts that as they travel to places in Mexico and Canada and see and maybe even drive these Chinese vehicles there will be increased pressure on U.S. automakers to make comparably priced EVs with comparable fuel efficiency and quality. There may also be pressure on the U.S. government to reduce Chinese import tariffs on EVs and hybrids.

Multiple Chinese auto makers besides BYP, including Zeekr, XPeng, NIO, and SAIC, are also producing popular EVs. Japanese auto makers are producing less expensive electric and hybrid vehicles as well. These Japanese models are surging in popularity in Europe and Asia.

It’s not only low-end vehicles coming out of Asia that are attracting attention and buyers. The AITO M9 (by Huawei and Seres) and the Zeekr 8X are direct, highly comparable Chinese alternatives to the BMW X5 plug-in hybrid (xDrive50e). These luxury SUVs offer extended-range or plug-in hybrid powertrains, massive all-electric ranges, and superior tech for a fraction of the price.

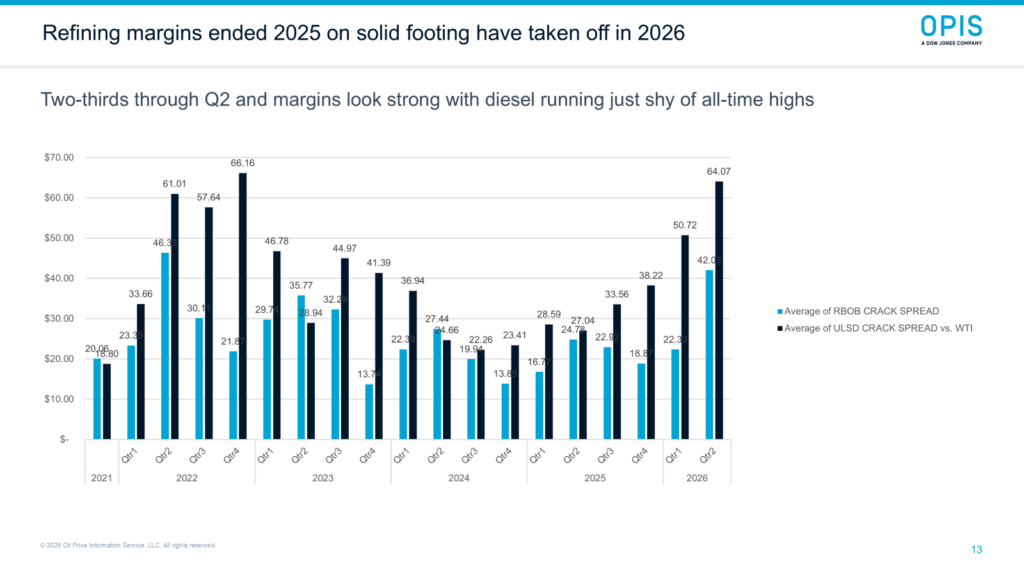

Refining margins in the U.S. right now are very good according to Cinquegrana (see his chart, below). Americans haven’t built a refinery since 1976, but existing refineries have expanded, creating greater capacity without necessitating new refinery construction. “Refining margins are good, there are plenty of outlets for the product that’s coming out of them, whether it’s domestic or international, to help fill gaps.”

To describe the ideal balance maintained in the oil industry, Cinquegrana uses a three bucket analogy: “You have three buckets of water in front of you, and they all have to stay even. When the first bucket gets really low, you have to take water from the other two buckets to even them all out. OPEC has for some time been the swing producer. In today’s climate, the U.S. refiner has taken over OPEC’s role and is making the swing product. That U.S. role as swing producer is elevated now due to the Iran war and Strait closure.” The three buckets Cinquegrana describes are The Americas, Europe, and Asia-Pacific.

A swing producer is the supplier with enough spare capacity and market influence to intentionally increase or decrease output and stabilize global prices. The swing producer absorbs the shock when supply and demand fall out of balance. Saudi Arabia and OPEC held that role for decades. When prices spiked, they opened the taps; when prices cratered, they cut production.

The U.S. refiner has effectively inherited that stabilizing role. This is not by choice, but by circumstance. Because domestic production is strong and the Strait is closed, the rest of the world is looking to U.S. refiners to fill gaps that the Middle East normally covers. The U.S. is topping up the other two buckets.

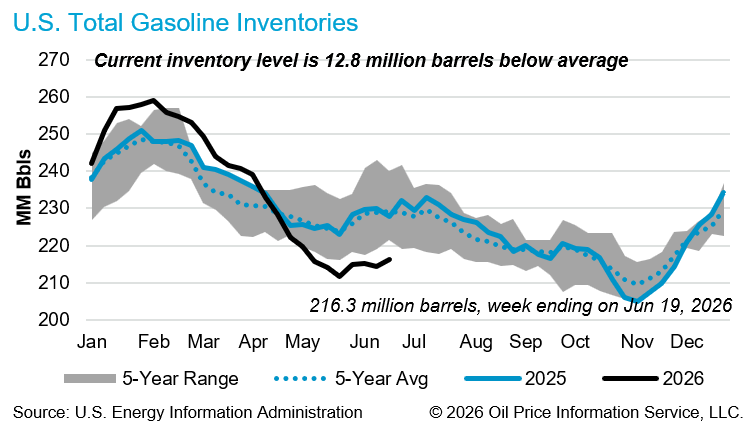

The catch is that OPEC managed that role deliberately and strategically. The U.S. is doing it reactively, and the system that enables it (pipeline capacity, storage, export infrastructure) is finite. If oil storage fills up and refineries pull back on production, the U.S. may not succeed in the role of swing producer. A country that acts as a swing producer by design works with a buffer, whereas a swing producer that is constantly reacting to circumstances is just running hard until something gives. “Gasoline inventories have dropped each of the last 14 weeks in the US. Now, granted, some of that in February and March was terminals kicking out the winter grade gasoline to make room for the summer grade, and usually we are trending lower this time of year, but if we don’t start to turn up in the next couple of weeks, then I’m really going to get concerned about fuel supplies for July and the rest of the summer,” shares Cinquegrana.

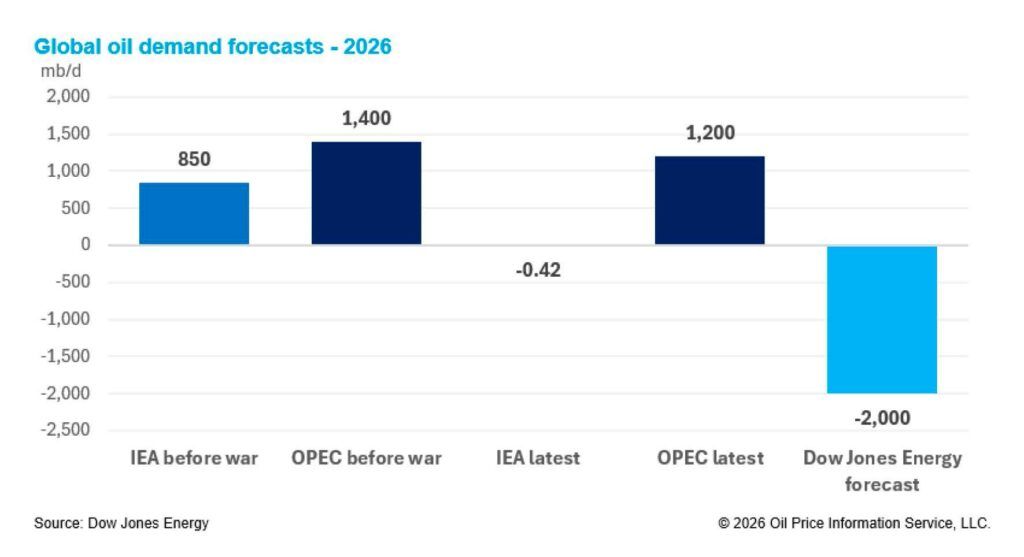

To address our current oil supply crisis, we need to look at how to increase supply and decrease demand. “We have a supply shock, and now we need a demand response,” says Cinquegrana. He describes how during COVID lockdowns there was a demand shock causing a supply response. “OPEC started producing less, U.S. futures started to back off from drill wells, and refineries reduced runs. Some refineries even transitioned to making biofuels, including two refineries in California: Phillips 66 at Rodeo and Marathon at Martinez did the same thing. So that was the supply response to a demand shock.” Now we have a supply shock, and we need the demand response. “We need to reduce global demand by 10 to 15 million barrels a day, or increase supply, but beyond the Strait opening, there’s not a clear path forward for an increase in supply.”

Because of the supply crunch, refineries are tapped in a way that’s unsustainable. “Refinery runs are creeping up in the U.S., where we’re now at nearly 92% of capacity. Capacity was down below 90% in April due to both planned and unplanned maintenance, so a ramp up at this time is mostly expected. But there is motivation to produce at a higher rate, because both domestic and international markets are strong,” says Cinqugrana. As we continue to work through the end of 2026, Cinquegrana and Rozell will continue to observe how refineries respond.

Cinquegrana would like to see the Strait open as soon as possible. As we have seen, opening the Strait will not instantly solve oil supply issues. “You have to get traffic traveling through the Strait again, refineries need to be restarted in the Gulf nations, Arab Gulf nations need to reposition their ships.” Many steps need to be taken.

When Cinquegrana talks about repositioning ships, he’s referring to very large crude carriers (VLCCs), which reverse at 13 knots per hour. This is the equivalent of 14 miles an hour. He describes this activity as akin to “riding a bike over water.” They don’t move very fast: repositioning these ships over to the Western Hemisphere to move crude oil takes a couple weeks. Then there are the oil production wells which will need official inspections to ensure there was no permanent damage to them during the war, and determine how long it will take before they are back up and running. “At that point, at the beginning of July, you’re at 18 weeks of war, it’ll take another 18 weeks for post-war normalization, so that takes you almost to the end of October before things normalize. If we do see resolution at the end of June, beginning of July, and then the 18 weeks for normalization, we’ll be okay.” Cinquegrana believes the impact will not be major if the oil market is back to pre-February productivity by October, however it is unclear if the current agreement will keep the Strait open for long given ongoing conflict between Israel and Lebanon.

That said, prices will not come down quickly. “We’re not going back to $57 WTI, like it was before the war, or $70 Brent. Prices are going to stay elevated.” This is, in part, because inventories will have been diminished during the conflict and replenishing inventories will be a priority for oil refiners. Additionally, oil-rich nations will focus on building more strategic reserves to prepare for future disruption.

Refineries hit by attacks during the conflict will also need time to rebuild. Parr paints a picture of what that looks like: “Twenty-five percent of Qatar’s production assets are offline from drone attacks right now. It will require multi-year projects to get those refineries up and running again, which means the whole global energy system is going to feel the effects of this war for an extended period of time.”

Cinquegrana sees this Strait closure and subsequent oil drought as a once-in-a-lifetime event. He considers the Russian invasion of Ukraine in 2022, but its effect on the cost of fuel world-wide is not comparable. “That example is imperfect because when Russia invaded Ukraine, oil prices shot up like a rocket and then dropped just as fast.” The market quickly saw that Russia was going to get their oil out to the marketplace despite sanctions. That 9 million barrels a day of oil production the industry thought would be cut off completely was only partially restricted. Russian production did decrease, but not enough to derail the whole oil market the way the Strait closure has.

When we spoke with Cinquegrana and Rozell, the national average retail gasoline price at its all-time high occurred in June 2022 in the months following Russia’s invasion of Ukraine. The price spike was $5.01 at the pump. This was the first time it had ever crossed $5 since AAA began collecting pricing data in 2000. Cinquegrana shared that he believed in H2 2026 we’d still potentially face that level of cost. That record has since been broken. The U.S. national average hit $5.12 per gallon in March, the new all-time record.

The forces shaping fuel markets in H2 2026 are unlike anything fleet operators have navigated in modern memory. The Iran war and the subsequent closure of the Strait of Hormuz did not just spike prices, these events exposed the structural limits of a global oil system that was already running lean on diesel inventories, refinery capacity, and storage. The U.S. refiner has stepped into a swing producer role it was not designed to hold, and the relief valve remains outside the oil industry’s direct control. Relief will come gradually once the Strait is re-opened, but only then.

What fleet managers can control is how they respond.

The operators who will finish 2026 strongest are likely those who do not simply wait for the re-opening of the Strait and hope for a return to normal. Fleet managers must evaluate their fuel spend against peers in their region and industry to find out how they might make their business more efficient. Successful fleet managers will tighten purchase controls now, because price volatility increases the chance of internal fraud. And operators must look closely at how they can transition to a mixed energy fleet. Hybrid and electric vehicles are now often less expensive than vehicles that run on gasoline or diesel, when taking in the total cost of ownership. In the current climate and going forward, cars and trucks that run without oil, or with only a minimal amount of oil, can be a major advantage to fleet companies.

When the war in Iran ends, prices are not likely to snap back to where they were. Even as the Strait of Hormuz reopened after the cease-fire agreement was signed in mid-June, less than half the number of ships move through it each day in comparison to before the start of the war, and the chances of re-closure are high. Once a more stable agreement is struck between Iran and the United States, inventories will need to be rebuilt. Nations that were caught exposed will prioritize strategic reserves, which will keep oil supplies limited for a longer period of time.

The fleet managers who come out ahead will likely be the ones who stop waiting for prices to return to normal, and start building operations resilient enough to perform regardless of what the market does next.

WEX is a leading, global fintech solutions provider, simplifying payments and back-end business processes in the fleet management, benefits management, and corporate payments areas. To learn more, please visit the company’s About WEX page.

Copyright ©2026 WEX Inc. All rights reserved. The information in this document is subject to change without notice. This article contains copyrighted material from Oil Price Information Service, LLC (“OPIS”), a Dow Jones Company, and is republished with explicit written permission.

Sources:

Recurrant

NPR

Power Magazine

National Insurance Crime Bureau

California Air Resources Board

Petroleum in Venezuela: A History

Wall Street Journal

New York Times

Sci Elo Brazil

International Affairs Review

AAA

Pump

Pew Research