Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

The IRS’ use-or-lose rule governs flexible spending accounts (FSAs). This rule is one of the big differentiators between FSAs and other types of employee benefits. So what is the use-or-lose rule? And what does it mean for the upcoming plan year? We’ll answer those questions and more.

A flexible spending account (FSA) is an employer-sponsored benefit that allows employees to set aside a portion of their pre-tax salary to pay for qualified medical expenses or dependent care expenses. These are designed to help participants save money on eligible out-of-pocket healthcare or childcare costs by reducing their taxable income. Participants decide how much to contribute to the FSA each year, and their funds can be used for a wide range of eligible expenses.

The IRS’ use-or-lose rule states that FSA funds must be spent by the participant within the FSA’s plan year. That means FSA participants typically need to spend most or all of their FSA funds by the end of the plan year. Unused funds at the end of the plan year are forfeited to the plan.

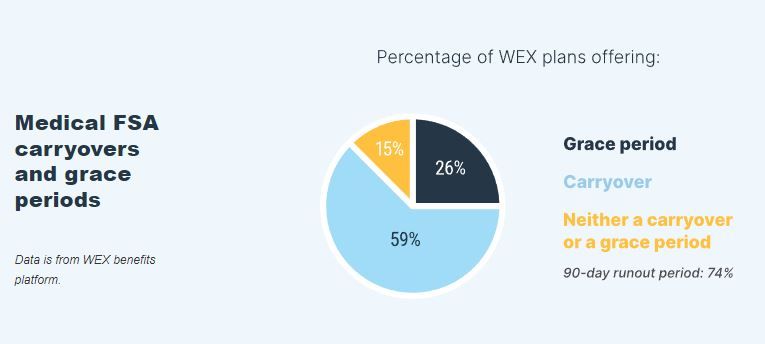

Possibly. The IRS normally allows up to a $660 carryover in 2025 of medical FSA funds from one plan year to the next. Employers determine whether their medical FSAs include a carryover.

A grace period is an extension of time beyond the end of the regular plan year in which FSA participants can incur new expenses and use any remaining funds from the previous plan year. This can last up to 2½ months after the end of the plan year.

The run-out period is a specific time frame after the end of the plan year in which FSA participants can submit claims for eligible expenses incurred during the plan year. Unlike a grace period, a run-out period does not allow for new expenses to be incurred during that period of time. A run-out period allows participants to request reimbursements for expenses they may have incurred close to the end of the plan year but haven’t submitted for reimbursement yet.

An employer can choose to offer either a grace period or a carryover, but not both. Sometimes, an employer may pick neither, which means any remaining funds in the FSA at the end of the plan year are forfeited.

Below, we’ve outlined what percentages of FSAs on the WEX benefits platform have a carryover or grace period. For more benchmarking data from our platform, click the graphic.

Usually, participants can only elect contributions to their FSA during open enrollment, but there are some exceptions where mid-year contributions are fine. This can include:

Yes. The IRS’ use-or-lose rule applies to medical FSAs and dependent care FSAs.

No. With a health savings account (HSA), all funds carry over from year to year. That’s one reason HSAs are “savings” accounts, while FSAs are “spending” accounts.

Would you like to learn more about medical FSAs? Check out our Benefits episode for a breakdown of eight things you should know about them.

This blog post originally published in December of 2021 and was most recently updated in August of 2025.

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own counsel.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.