Health Savings Accounts (HSA), Open Enrollment, Participants

WEX Health

HSAs, Open enrollment

Share

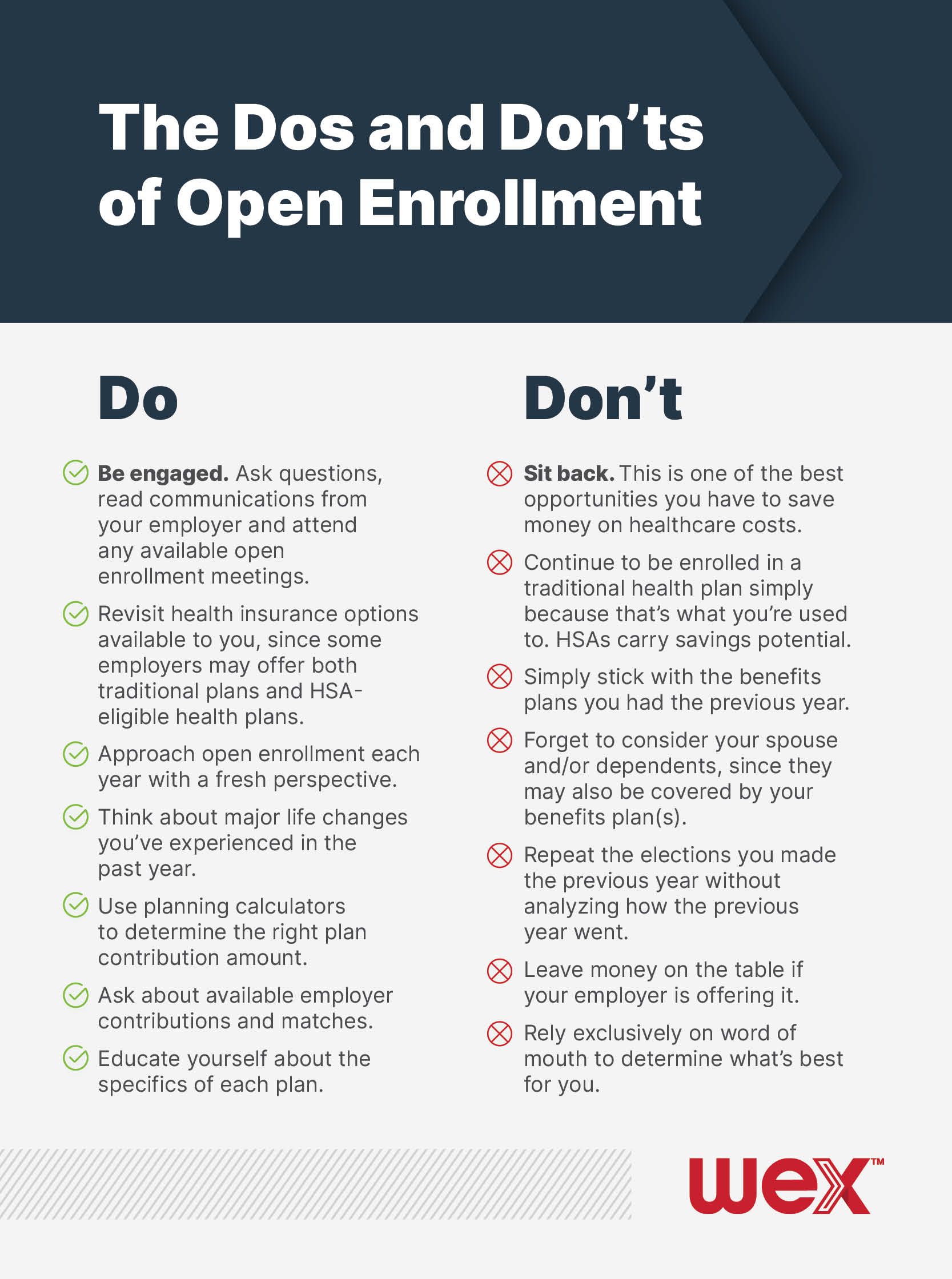

Open enrollment is around the corner for many of you. It’s your best chance to evaluate your healthcare needs and identify opportunities to better support yourself and your family. However, a whopping 92 percent of employees stick with the same elections they had the previous year, no matter what changes have taken place in their lives. If you’re one of that majority, you may be missing out on multiple ways to save, either through the health plan you choose or through the benefits you enroll in. Fortunately, a few open enrollment tips can go a long way to making sure you’re maximizing your savings potential.

When approaching open enrollment, do …

Evaluate available health insurance plans. Increasingly, employers are offering their employees both HSA-eligible health plans (or high-deductible health plans) and traditional health plans. If you rarely go to the doctor or would like to enroll in a health savings account (HSA), an HSA-eligible health plan may be right for you!

Consider any major life changes you and your family have experienced in the previous year. For example, do you have any new dependents who have healthcare needs and could be covered by a pre-tax benefits plan? Will anyone in your family have anticipated healthcare costs in the upcoming year?

Engage in opportunities to learn more about available plans. Nearly three-quarters of all employees say they don’t understand some components of their benefits. This is your best opportunity to discuss available plans with your employer and learn what has changed from the previous year.

Let money your employer is offering go unclaimed. If your employer offered you a raise, you wouldn’t say no, right? That’s essentially what you’re doing when your employer offers to contribute or match your contributions to a benefits plan or 401(k) and you’re not taking advantage.

Miss out on learning opportunities. The “daily grind” can often get in the way of the big picture, but don’t let it! Open enrollment comes just once a year.

Treat your approach to benefits plans the same when making open enrollment decisions. For example, a medical flexible spending account (FSA) is governed by the IRS’ use-or-lose rule, so it’s important that you choose the right contribution amount each year or risk losing money at the end of the plan year. On the other hand, all HSA funds carry over from year to year, so there’s less risk and more reason to contribute as much as you can, up to the contribution limit set by the IRS.

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.